Sector Watch 2023 📈

Sector Watch 2023 📈

What are the most exciting sectors for your portfolio this year?

2022 was a year like no other.

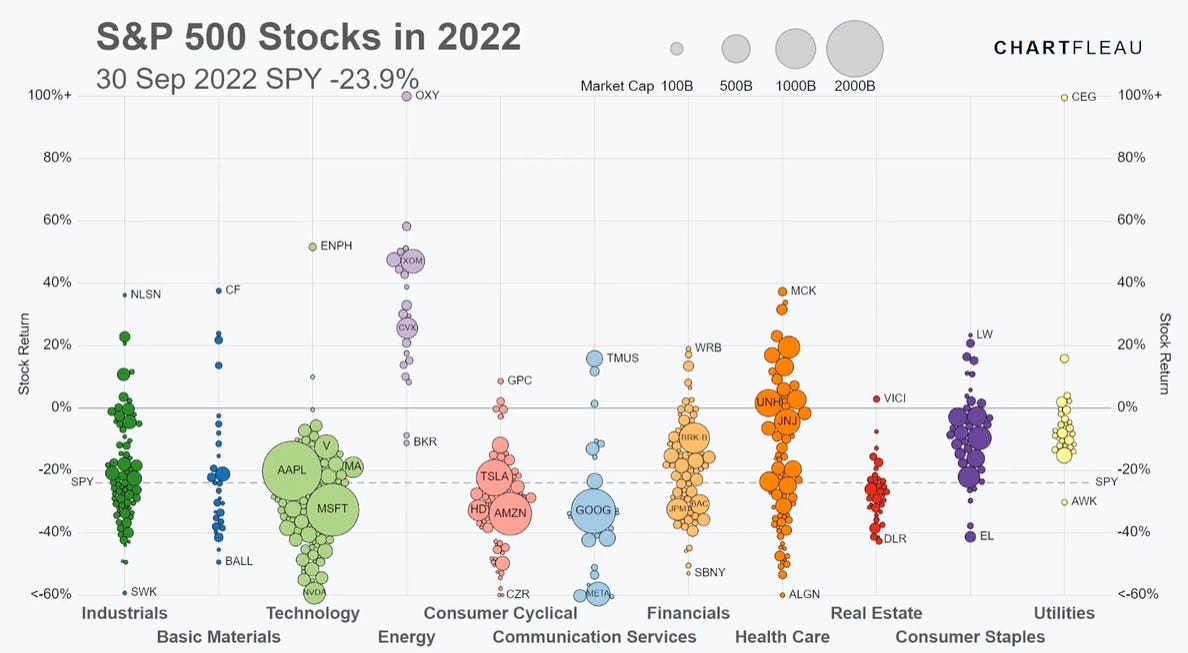

What worked in 2022? 📈

We had as many one in a generation events to contend with when making investments as in recent memory, as macroeconomics, geopolitics, and uncertainty ran amok.

Many other sectors saw growth, as experienced investors flocked from the high valuations and speculation in tech companies, looking to safe haven, reliable companies who have weathered the same storms over and over again.

The rise of mRNA vaccines during the pandemic also opened the potential for further success in other diseases, leading to a rise in the investment in medical distribution and manufacturing.

As we’d expect with war in Europe, the Defence sector saw major gains, as countries looked to ramp up their arsenals, and ensure their defensive capabilities were sufficient for any potential escalations.

Unfortunately not every sector was so lucky; the technology sector was hammered by the prospect, and then reality, of rising interest rates, hitting the cost of capital, and hampering future profits.

Anything with a high P/E was in big trouble, especially if making losses, and when combined with constraints to supply chains, and geopolitical tensions globally, most sectors saw extensive drawdowns.

Of course, understanding all this is easy after the fact, but that’s not what investing is all about. What we really care about is the next 12 months, so which of the S&P’s 11 sectors should we be looking at?

Of course many people expect a recession to arrive some time in 2023, but with so much forecasting and expectation, much of this pain may well be priced into the markets.

Whether the second leg down comes when the hit to the wider economy comes, causing major declines in demand for goods and services as businesses tighten their belts, and make the difficult decision to lay off staff.

For me, the 5 key questions for the next 12 months are as follows:

How will inflation trend as central banks continue with rate hikes, and what happens when this stops?

How will the conflict in Ukraine play out, and will a peaceful resolution be reached?

Will layoffs in the tech sector spread into other areas of the economy?

How will the property sector behave as the hybrid working model normalises?

How will China’s reopening impact inflation and supply chains?

So onto my sectors to keep an eye on in the next year… 👀

Health

Energy

Utilities

Industrial

Health 🏥

Regardless of what is going on in the economy, if you have a medical issue, it's a priority. This ensures there is a reliable base of revenue for companies in the sector, as well as a long runway and pricing control, but also some prospect for growth as we expect a growing, and ageing population in most developed countries.

Most investors consider the sector to be fairly defensive as a result, since performance can be relied upon in a wider range of economic and geopolitical outcomes, especially in the event of a recession, where governments are incentivised to step in if performance is declining, unlike in some other areas of the market.

With a split congress in the US, and the Inflation Reduction Act now approved, it is unlikely that we see any sweeping new legislation which may negatively impact the sector.

However, the sector can be relied upon to provide innovation despite this level of stability, with incredible breakthroughs in genetics showing us glimpses of the future of healthcare.

Risk- I’d consider the major risk in the sector to be that investors opt for a more offensive strategy as inflation declines, rotating out of defensive sectors and into speculative sectors which may see better returns in a bullish market.

Energy ⚡️

One of the most notoriously difficult sectors to predict is the energy sector. As with many other sectors, we will always need some form of energy regardless of the economy, but with fluctuating oil prices, and the eventual transition to renewable energy sources, establishing the value of individual stocks can be a real challenge.

However, with 2022 being such a fantastic year for the sector, and with many of the same challenges still present in 2023, such as several years of low production, and constraints on Russian oil and gas, I suspect the sector will continue to perform well, in particular those at the upstream end of extraction and exploration, due to the long lead time for counties to re-balance their oil and gas supplies.

The renewable component also presents a challenge for investors, as sky high valuations mean the excitement around these companies has already priced out many value investors.

Risk- The key risk I see to the sector is the potential for a recession, which could drastically lower demand for fuel and electricity.

Utilities ⛽️

The consumers of most developed economies have some clear demands from futures governments, mostly around climate change and a shift away from fossil fuels.

It is clear that decarbonisation is going to play a huge role in the coming decades, as most countries move from fossil fuel dominant to an electricity based utility sector.

Making the infrastructure transition from fossil fuel based generation, heating, vehicle fuelling, and many other areas will not be a small task. The Inflation Reduction Act and Infrastructure Act have started the ball rolling here, with extensive investment being made at a government level.

The sector performed well in 2022, and despite being one of the less exciting areas in terms of innovation, if performance and defensive positioning is your goal; this could be the place.

I like the sector for a variety of reasons in 2023. If we see a recession, then I expect most businesses and homes to still demand the same level of utility coverage, as well as continued progress towards carbon neutrality.

If there is not a recession, then I expect governments to push more aggressively towards a greener grid, meaning that both outcomes will lead to steady growth in the sector.

Industrials 🏭

In the same trend, consumers are demanding that manufacturing is brought into domestic control amid security and geopolitical tensions.

With governments assisting in this transition, there is tremendous potential for long overdue developments in the decarbonisation, sustainability, and stability of the sector.

Such long term plans from central governments mean that short term market movements are less significant, making the sector an excellent defensive choice.

Conclusion

2023 is definitely going to be the year of the stock picker.

No longer can we rely on an ‘everything rally’, with near to zero interest rates, and easy money borrowing long gone.

I expect the companies which can provide goods or services which we all need will dominate, and if you can find those executing well, and fairly priced, you might be into a winner.

What do you think will be the winners of 2023?