The Acorn #36🌳

The Acorn #36🌳

All you need to understand the market this week

Monday, July 24th 2023

Hi Oak Investors,

Welcome to another recap on the week’s action and events!

At Oak Investing, I look to provide value for all levels of investor, whether it’s pulling together the week’s best articles, insights and breaking news, or clarifying new concepts for beginners.

I hope you enjoy this week’s recap, please get in touch if there’s anything more you’d like to see in The Acorn. If you like what you see, please like, subscribe and share to keep growing the Oak Investor community! 🌳

Thanks,

Gordon

Summary 📝

Last week was a story of two halves, as markets continued their rally until earnings from Tesla and Netflix disappointed, leading to a slight decline towards the end of the week.

The S&P 500 gained 0.61%, NASDAQ dropped 0.42%, and the Dow Jones Industrial Average climbed 2%.

The Volatility Index crept up as investors were disappointed by Elon Musk’s hinting at further price cuts, and Netflix earnings guidance. The VIX remains under 20, indicating that volatility is still fairly low, so now may be a decent time to take advantage of any disappointments in earnings reports coming this week!

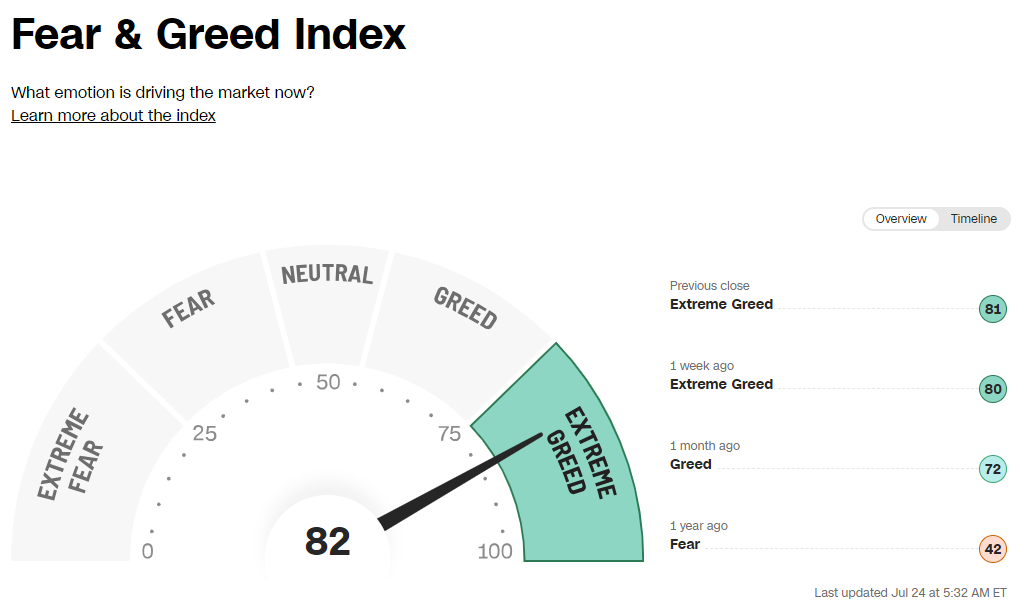

The Fear and Greed index remained in the Extreme Greed category at 82/100.

This Week in History 📰

Provided by The History Place

July 25, 1909 - The world's first international overseas airplane flight was achieved by Louis Bleriot in a small monoplane.

July 26, 1953 - The beginning of Fidel Castro's revolutionary "26th of July Movement."

July 27, 1953 - The Korean War ended with the signing of an armistice by U.S. and North Korean delegates at Panmunjom, Korea.

Major Events This Week 🔬

Economic Events (EST)

Provided by Unusual Whales

Monday

9:45 am S&P "flash" U.S. manufacturing PMI

9:45 am S&P "flash" U.S. services PMI

Tuesday

9:00 am S&P Case-Shiller home price index (20 cities)

10:00 am Consumer confidence

Wednesday

10:00 am New home sales

2:00 pm FOMC decision on interest-rate policy

2:30 pm Fed Chairman Powell press conference

Thursday

8:30 am Initial jobless claims

8:30 am Durable-goods orders

8:30 am Durable-goods minus transportation

8:30 am GDP (advanced report)

8:30 am Advanced U.S. trade balance in goods

8:30 am Advanced retail inventories

8:30 am Advanced wholesale inventories

10:00 am Pending home sales

Friday

8:30 am Personal income (nominal)

8:30 am Personal spending (nominal)

8:30 am PCE index

8:30 am Core PCE index

8:30 am PCE (year-over-year)

8:30 am Core PCE (year-over-year)

8:30 am Employment cost index

10:00 am Consumer sentiment (final)

Incoming Earnings Reports

Provided by Earnings Whispers

Notable Upcoming Earnings

Provided by Unusual Whales

Monday

DPZ (premarket) Implied move: +/- 4.91% Sector: Consumer Cyclical

CLF (afterhours) Implied move: +/- 6.23% Sector: Basic Materials

LOGI (afterhours) Implied move: +/- 6.54% Sector: Technology

Tuesday

GM (premarket) Implied move: +/- 4.38% Sector: Consumer Cyclical

VZ (premarket) Implied move: +/- 3.69% Sector: Communication Services

GE (premarket) Implied move: +/- 3.97% Sector: Industrials

MMM (premarket) Implied move: +/- 3.81% Sector: Industrials

SPOT (premarket) Implied move: +/- 9.00% Sector: Communication Services

GOOGL (afterhours) Implied move: +/- 5.15% Sector: Communication Services

MSFT (afterhours) Implied move: +/- 4.98% Sector: Technology

SNAP (afterhours) Implied move: +/- 18.84% Sector: Communication Services

V (afterhours) Implied move: +/- 2.86% Sector: Financial Services

TXN (afterhours) Implied move: +/- 3.85% Sector: Technology

TDOC (afterhours) Implied move: +/- 11.40% Sector: Healthcare

Wednesday

T (premarket) Implied move: +/- 4.83% Sector: Communication Services

KO (premarket) Implied move: +/- 1.74% Sector: Consumer Defensive

BA (premarket) Implied move: +/- 4.09% Sector: Industrials

TLRY (premarket) Implied move: +/- 12.12% Sector: Healthcare

META (afterhours) Implied move: +/- 8.49% Sector: Communication Services

EBAY (afterhours) Implied move: +/- 4.68% Sector: Consumer Cyclical

NOW (afterhours) Implied move: +/- 5.66% Sector: Technology

CMG (afterhours) Implied move: +/- 5.70% Sector: Consumer Cyclical

Thursday

ABBV (premarket) Implied move: +/- 3.36% Sector: Healthcare

MA (premarket) Implied move: +/- 2.90% Sector: Financial Services

MCD (premarket) Implied move: +/- 2.42% Sector: Consumer Cyclical

F (afterhours) Implied move: +/- 4.82% Sector: Consumer Cyclical

INTC (afterhours) Implied move: +/- 6.16% Sector: Technology

X (afterhours) Implied move: +/- 5.69% Sector: Basic Materials

ROKU (afterhours) Implied move: +/- 10.90% Sector: Communication Services

Friday

XOM (premarket) Implied move: +/- 2.56% Sector: Energy

CVX (premarket) Implied move: +/- 2.49% Sector: Energy

AZN (premarket) Implied move: +/- 2.64% Sector: Healthcare

PG (premarket) Implied move: +/- 2.57% Sector: Consumer Defensive

Friday

AXP (premarket) Implied move: +/- 3.1% Sector: Financial Services

Post of the Week 💌

✅ With today’s release of Barbie and Oppenheimer, the craze of combining the two is going to be the debate of the week. But if the two were investors, which companies would they be interested in? 🤔

✅ I asked Chat-GPT which companies Barbie and JR Oppenheimer would likely invest in today. What do you think of ‘their’ picks? 💰

What’s Moving Markets? 🏃♂️

Three stories I’m watching carefully this week. Provided by CNBC

A ‘momentous week’ ahead as the Fed, ECB and Bank of Japan near pivot point

The market is pricing 25 basis point hikes for the Federal Reserve and the European Central Bank, but economists will be closely scrutinizing communications on their future rate paths.

The Bank of Japan faces a different challenge, and is expected to keep its -0.1% short-term interest rate target despite inflation consistently exceeding target and signs of the economy heating up.

China has announced a slew of measures to bolster its economy. Here’s what we know so far

A key Politburo meeting later this week will review China’s economic performance in the first half of the year.

Ahead of that meeting, China has pledged to optimize the business environment for private enterprises.

Beijing announced measures to bolster consumption, particularly for household products and electric vehicles.

A 10-year rally in U.S. home prices could be coming to an end, says Yale’s Robert Shiller

A decade-long rally in U.S. home prices could finally come to an end once the Federal Reserve stops its rate-hiking cycle, said Robert Shiller, professor of economics at Yale University.

Home prices have made steady gains since 2012, according to the S&P Case-Shiller U.S. National Home Price Index.

“The fear of interest rate increases has influenced people’s thinking — it’s not just the homeowners, it’s new buyers who wanted to get in before the interest rates went up even more,” Shiller said.

Chart of the Week 📈

Provided by Chart of the Day

Rising interest rates, losses on commercial real estate and heightened regulatory scrutiny will pressure regional and midsized banks, leading to a wave of mergers, sources told CNBC.

Some of those pressures will be visible as regional banks disclose second-quarter results this month. Firms already have warned of sinking revenues.

And according to one analyst, half the country’s banks will likely be swallowed by competitors in the next decade.

Investor’s Toolkit ⚒️

Unusual Whales- Options Flow and Analysis 🛠

5% off with code OAK2022

SimplyWallSt- Stock Analysis 🛠

5% Discount with code OAK

Want to Work with Me? 📈

If you’d like to take your investing to the next level, there are 3 ways I can help:

Pick up a copy of The Investor’s Blueprint, and learn at your own pace 📚

Book a free discovery call with me, and discuss how you can take a step closer to financial freedom 🏆

Follow me on social media, for daily financial education and market insights. 👏

Follow for More 🎉

Thanks for reading, have a great day!

Gordon

Disclosure ✅

This newsletter provides general information only. Before making any financial or investment decisions, please consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.