The Acorn #41

The Acorn #41

All you need to understand the market this week

Monday, August 28th 2023

Hi Oak Investors,

Welcome to another recap on the week’s action and events!

At Oak Investing, I look to provide value for all levels of investor, whether it’s pulling together the week’s best articles, insights and breaking news, or clarifying new concepts for beginners.

I hope you enjoy this week’s recap, please get in touch if there’s anything more you’d like to see in The Acorn. If you like what you see, please like, subscribe and share to keep growing the Oak Investor community! 🌳

Thanks,

Gordon

Summary 📝

Another WILD week in the market as Nvidia reported another bumper earnings, and as Fed Chair Jerome Powell commented on the progress towards inflation cooling, and the state of the economy.

The S&P 500 rose 0.6%, NASDAQ climbed 1.8%, and the Dow Jones Industrial Average fell 0.53%.

The Volatility Index dropped as the potential for surprises in J.Powell’s speech, and in Nvidia earnings passed without event. As we’ve seen for a while, the market is ready for a signal for which direction to go next. A bad report by Nvidia, or surprise comments from the Fed could’ve easily sent us down in a big way this week.

I suspect more sideways moves will be likely as the market progresses through the next few weeks of seasonally poor performance, with a view to picking up towards the end of the year.

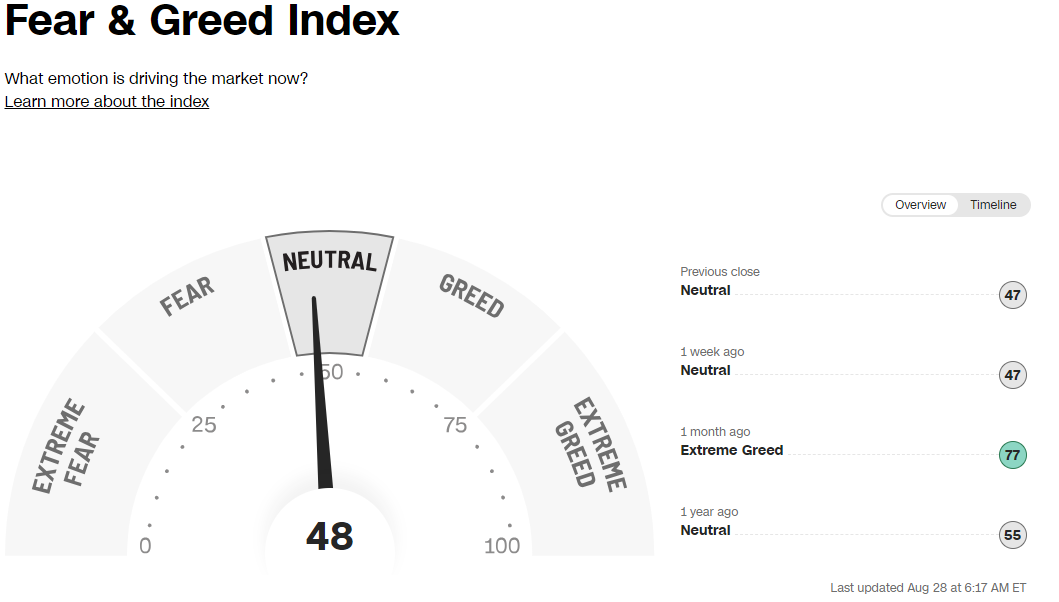

The Fear and Greed index remained in the neutral category, slightly within the neutral range at 48/100.

As I noted last week, with August being a seasonally poor month for the market, I like the idea of putting some cash to work here.

There may be some more bumps in the road, particularly in September, but we’re looking to catch the majority of the market growth, rather than trying to time the market exactly.

As always, keep to your strategy, don’t let the noise change your plan, and learn as much as you can!

This Week in History 📰

Provided by The History Place

August 28, 1963 - The March on Washington occurred as over 250,000 persons attended a Civil Rights rally in Washington, D.C., at which Rev. Dr. Martin Luther King, Jr. made his now-famous I Have a Dream speech.

{kind=link}

{kind=link}

September 2, 1666 - The Great Fire of London began in a bakery in Pudding Lane near the Tower.

September 3, 1939 - Great Britain and France declared war on Germany after its invasion of Poland two days earlier.

Major Events This Week 🔬

Economic Events (EST)

Provided by Unusual Whales

Tuesday

9:00 am S&P Case-Shiller home price index (20 cities)

10:00 am Job openings

10:00 am Consumer confidence

Wednesday

8:15 am ADP employment

8:30 am GDP (revision)

8:15 am ADP employment

8:30 am Advanced retail inventories

8:30 am Advanced wholesale inventories

10:00 am Pending home sales

Thursday

8:30 am Initial jobless claims

8:30 am Personal income (nominal)

8:30 am Personal spending (nominal)

8:30 am PCE index

8:30 am Core PCE index

8:30 am PCE (year-over-year)

8:30 am Core PCE (year-over-year)

9:45 am Chicago Business Barometer

Friday

8:30 am U.S. nonfarm payrolls

8:30 am U.S. unemployment rate

8:30 am U.S. hourly wages

8:30 am Hourly wages year over year

10:00 am ISM manufacturing

10:00 am Construction spending

Incoming Earnings Reports

Provided by Earnings Whispers

Notable Upcoming Earnings

Provided by Unusual Whales

Notable Upcoming Earnings

Monday

HEI (afterhours) Implied Move: +/- 4.11% Sector: Industrials

Tuesday

NIO (premarket) Implied Move: +/- 8.44% Sector: Consumer Cyclical

PDD (premarket) Implied Move: +/- 8.55% Sector: Consumer Cyclical

BBY (premarket) Implied Move: +/- 5.70% Sector: Consumer Cyclical

HPQ (afterhours) Implied Move: +/- 4.43% Sector: Technology

Wednesday

CRM (afterhours) Implied Move: +/- 6.10% Sector: Technology

CRWD (afterhours) Implied Move: +/- 7.59% Sector: Technology

CHWY (afterhours) Implied Move: +/- 11.91% Sector: Consumer Cyclical

Thursday

DG (premarket) Implied Move: +/- 6.77% Sector: Consumer Defensive

UBS (premarket) Implied Move: +/- 6.06% Sector: Financial Services

AVGO (afterhours) Implied Move: +/- 6.44% Sector: Technology

VMW (afterhours) Implied Move: +/- 5.08% Sector: Technology

LULU (afterhours) Implied Move: +/- 7.59% Sector: Consumer Cyclical

MDB (afterhours) Implied Move: +/- 11.91% Sector: Technology

Post of the Week 💌

✅ Most of your investments are probably held in some of the biggest companies we all know and love, but how often do you explore new markets and new sectors? 🤔

✅ Over the last few years, the BRICS has been an interesting areas of focus. With international markets outperforming the S&P in 2022, we might start to see an area of real untapped potential in some of these.📈

✅ News broke today that 6 new countries are expected to join the group, expanding trade and cooperation between the countries. This will likely have large political consequences, but presents some interesting investment opportunities also. 🤔

✅ Investing directly in these markets may be more complex with OTC markets, but plenty of great companies with exposure to these market are traded on the NYSE and LSE.

Have you ever invested in BRICS companies? Let us know 🤔🤔

What’s Moving Markets? 🏃♂️

Three stories I’m watching carefully this week. Provided by CNBC

U.S.-India relationship has reached new heights as the two align across policy areas, USTR says

U.S. Trade Representative Katherine Tai said the U.S.-India relationship is reaching new heights as the two align “across all the policy areas.”

China’s rare earths dominance makes U.S. supply chains vulnerable, trade representative says

China’s dominance in rare earths makes U.S. supply chains vulnerable, U.S. Trade Representative Katherine Tai said in an exclusive interview Saturday with CNBC’s Martin Soong.

Tai was speaking in New Delhi, India, on the sidelines of B20, the official business dialogue forum of the G20.

“What I want to draw your attention to is not just the vulnerabilities around China’s investments [overseas], but the fact that China’s dominant position in the world market now in [rare earths] means that it is able to turn on the faucet and turn off the faucet,” she said.

China’s industrial profits extend slump into seventh month

Profits at China’s industrial firms fell 6.7% in July from a year earlier, extending this year’s slump to a seventh month with weak demand squeezing companies as a post-pandemic recovery faltered in the world’s second-biggest economy.

")

Chart of the Week 📈

Provided by Chart of the Day

Wall Street is really suffering through the dog days of August.

The Nasdaq Composite is also headed for its biggest one-month loss since December, falling 5.2%. The Dow Jones Industrial Average has declined 3% this month, and the S&P 500 is down more than 3% this month, on pace to snap a five-month winning streak.

The broader market index is also on track to post its worst monthly performance since December, when it lost 5.9%.

There are several things pressuring Wall Street now, ranging from seasonal factors to concerns about the global economy and the Federal Reserve.

Investor’s Toolkit ⚒️

Unusual Whales- Options Flow and Analysis 🛠

5% off with code OAK2022

SimplyWallSt- Stock Analysis 🛠

5% Discount with code OAK

Want to Work with Me? 📈

If you’d like to take your investing to the next level, there are 4 ways I can help:

Pick up a copy of The Investor’s Blueprint, and learn at your own pace 📚

Book a free discovery call with me, and discuss how you can take a step closer to financial freedom 🏆

Check out my regular articles on Motley Fool UK 📚

Follow me on social media, for daily financial education and market insights. 👏

Follow for More 🎉

Thanks for reading, have a great day!

Gordon

Disclosure ✅

This newsletter provides general information only. Before making any financial or investment decisions, please consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.