The Acorn 🌳#51

The Acorn 🌳#51

All you need to understand the market this week 📈

Monday, November 20th 2023

Hi Oak Investors,

Welcome to another recap on the week’s action and events!

At Oak Investing, I look to provide value for all levels of investor, whether it’s pulling together the week’s best articles, insights and breaking news, or clarifying new concepts for beginners.

I hope you enjoy this week’s recap, please get in touch if there’s anything more you’d like to see in The Acorn. If you like what you see, please like, subscribe and share to keep growing the Oak Investor community! 🌳

Thanks,

Gordon

Sponsor 🤝

This week’s newsletter is brought to you by Shares.io.

Become a smarter investor with Shares. Access more than 1,500 US stocks and connect with fellow investors.

This is a promotional content from which I may earn a commission. T&Cs and fees apply. Capital at risk.

Summary 📝

Yet ANOTHER generously green week across the market as CPI data from the US hinted that the war against inflation may finally be coming to an end!

S&P 500- 2.43%

NASDAQ- 2.79%

Dow Jones Industrial Average- 1.99%

The Volatility Index continued to slide as fears of further rate hikes were priced out.

At present, markets are pricing in a 99.8% chance of no change in rates at the next Fed meeting in mid December, with a 0.2% chance of 25BPS cut.

October’s US CPI data showed us that the cost of goods continues to slow in price increases. With the influential “shelter” component of the CPI still to materially come down, there is still a lot more decline to come for this, even if the Fed does nothing.

I suspect there won’t be any further rate hikes, but the Fed STILL need to remain firm in their language to prevent inflation from surging back.

The Fear and Greed index climbed back into the Greed category for the first time since September at 58/100.

It’s a short week for the market at Thanksgiving takes over in the US, so be conscious of the volatility that may come from low volume and new market opening and closing times!

As I noted last week, seasonality is never far from my mind at this time of year, and it looks like the market is thinking the same thing despite some negative headlines. The average across the last 20 years has been great for the next few months, and many institutions seemingly don’t want to miss out!

Of course, nothing is a guarantee these days, but as always, if you keep to your strategy, don’t let the noise change your plan, and learn as much as you can, you can’t go too wrong over the long term!

This Week in History 📰

Source- The History Place

November 20, 1947 - England's Princess Elizabeth married Philip Mountbatten.

November 20, 1962 - The Cuban Missile Crisis concluded as President John F. Kennedy announced he had lifted the U.S. Naval blockade of Cuba.

November 21, 1783 - The first free balloon flight took place in Paris as Jean Francois Pilatre de Rozier and Marquis Francois Laurent d'Arlandes ascended in a Montgolfier hot air balloon.

What’s on my Watchlist? 👀

Three stocks I think have an interesting week ahead.

$MSFT- With the latest drama on OpenAI, the company could quickly take the lead in the fight for AI dominance. 🤖

$BABA- If relations between the US and China can improve, this undervalued giant could be a big winner. 🏆

$NVDA- With earnings this week, the company needs to keep its momentum going, or investors could be majorly disappointed. 📈

What’s Moving Markets? 🏃♂️

Three stories I’ve got my eye on this week. Sourced from CNBC.

Ousted OpenAI head Sam Altman to lead Microsoft’s new AI team

OpenAI’s board announced late Friday that it was removing Altman and replacing him on an interim basis with technology chief Mira Murati.

Then late Sunday night, OpenAI said it was bringing on board former Twitch CEO Emmett Shear to run the artificial intelligence company.

And just hours after, the story took another twist with Nadella announcing that Altman and Brockman would be absorbed in-house into the Microsoft team.

CEO Summit in San Francisco, California, U.S. November 16, 2023. REUTERS/Carlos Barria")

U.S., China will seek to limit rising tensions amid domestic challenges, risk analyst says

Xi and Biden met last week for the first time in a year, on the sidelines of this year’s Asia Pacific Economic Cooperation leaders’ meeting in San Francisco.

They agreed to resume high level military communication between two countries that were halted after bilateral relations were derailed by a stray surveillance balloon that drifted over continental U.S. early this year and ex-House Speaker Nancy Pelosi’s Taiwan visit in August 2022.

Leaders' week in Woodside, California on November 15, 2023.")

Argentina elects ‘shock therapy’ libertarian Javier Milei as president

party, speaks at the campaign closing event on Oct.18, 2023.")

Official results showed Milei with near 56% votes versus 44% for his rival, Peronist Economy Minister Sergio Massa.

Milei is pledging economic shock therapy including shutting the central bank, ditching the peso, and slashing spending.

Milei will have to deal with a $44 billion debt program with the International Monetary Fund, inflation nearing 150% and a dizzying array of capital controls.

Major Events This Week 🔬

Economic Events

Source- Unusual Whales

Monday

10:00 am U.S. leading economic indicators

12:00 pm Richmond Fed President Tom Barkin TV appearance

Tuesday

10:00 am Existing home sales

2:00 pm Minutes of Fed's Oct. 31-Nov. 1 FOMC meeting

Wednesday

8:30 am Initial jobless claims

8:30 am Durable-goods orders

8:30 am Durable-goods minus transportation

10:00 am Consumer sentiment (final)

Thursday

Thanksgiving- US Markets closed

Friday

9:45 am S&P flash U.S. services PMI

9:45 am S&P flash U.S. manufacturing PMI

Incoming Earnings Reports

Source- Earnings Whispers

Notable Upcoming Earnings

Monday

TCOM (premarket) Implied Move: +/- 7.55% Sector: Consumer Cyclical

ZM (afterhours) Implied Move: +/- 7.87% Sector: Communication Services

A (afterhours) Implied Move: +/- 6.91% Sector: Healthcare

Tuesday

IQ (premarket) Implied Move: +/- 7.95% Sector: Communication Services

BIDU (premarket) Implied Move: +/- 5.62% Sector: Communication Services

KSS (premarket) Implied Move: +/- 10.80% Sector: Consumer Cyclical

BBY (premarket) Implied Move: +/- 6.07% Sector: Consumer Cyclical

LOW (premarket) Implied Move: +/- 3.78% Sector: Consumer Cyclical

DKS (premarket) Implied Move: +/- 8.03% Sector: Consumer Cyclical

NVDA (afterhours) Implied Move: +/- 6.67% Sector: Technology

HPQ (afterhours) Implied Move: +/- 5.04% Sector: Technology

JWN (afterhours) Implied Move: +/- 11.55% Sector: Consumer Cyclical

ADSK (afterhours) Implied Move: +/- 5.61% Sector: Consumer Cyclical

Wednesday

DE (premarket) Implied Move: +/- 4.13% Sector: Industrials

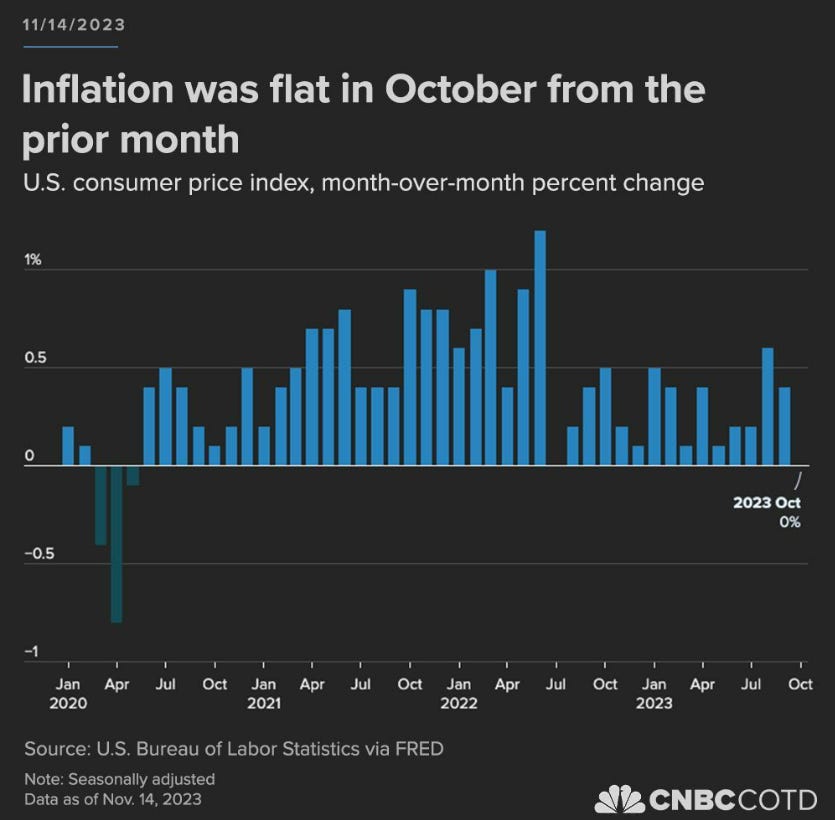

Chart of the Week 📈

Source- Chart of the Day

Inflation was flat in October from the previous month, providing a hopeful sign that stubbornly high prices are easing their grip on the U.S. economy and giving a potential green light to the Federal Reserve to stop raising interest rates.

The consumer price index, which measures a broad basket of commonly used goods and services, increased 3.2% from a year ago despite being unchanged for the month, according to seasonally adjusted numbers from the Labor Department on Tuesday. Economists surveyed by Dow Jones had been looking for respective readings of 0.1% and 3.3%.

Investor’s Toolkit ⚒️

Unusual Whales- Options Flow and Analysis 🛠

5% off with code OAK2022

SimplyWallSt- Stock Analysis 🛠

5% Discount with code OAK

Want to Work with Me? 📈

If you’d like to take your investing to the next level, there are 4 ways I can help:

Pick up a free 40 page copy of It’s Only Investing, and get started with investing! 📚

Pick up the comprehensive, 150 page The Investor’s Blueprint, and learn at your own pace 📚

Book a free discovery call with me, and discuss how you can take a step closer to financial freedom 🏆

Check out my regular articles on Motley Fool UK 📚

Follow me on social media, for daily financial education and market insights. 👏

Follow for More 🎉

Thanks for reading, have a great day!

Gordon

Disclosure ✅

This newsletter provides general information only. Before making any financial or investment decisions, please consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.

Critical moment for the market, does the Santa rally continue or has it reached its peak?