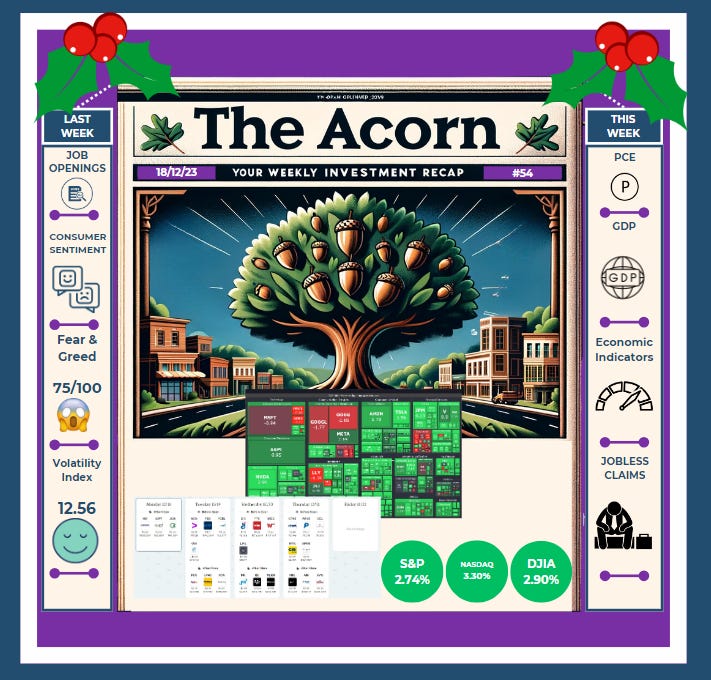

The Acorn 🌳#54

The Acorn 🌳#54

All you need to understand the market this week 📈💰👀

Monday, December 18th 2023

Hi Oak Investors,

Welcome to another recap on the week’s action and events!

At Oak Investing, I look to provide value for all levels of investor, whether it’s pulling together the week’s best articles, insights and breaking news, or clarifying new concepts for beginners.

I hope you enjoy this week’s recap, please get in touch if there’s anything more you’d like to see in The Acorn. If you like what you see, please like, subscribe and share to keep growing the Oak Investor community! 🌳

Thanks,

Gordon

Sponsor 🤝

This week’s newsletter is brought to you by Shares.io.

Become a smarter investor with Shares. Access more than 1,500 US stocks and connect with fellow investors.

This is a promotional content from which I may earn a commission. T&Cs and fees apply. Capital at risk.

Want to Work with Me? 📈

If you’d like to take your investing to the next level, there are 4 ways I can help:

Pick up a free 40 page copy of It’s Only Investing, and get started with investing! 📚

Pick up the comprehensive, 150 page The Investor’s Blueprint, and learn at your own pace 📚

Book a free discovery call with me, and discuss how you can take a step closer to financial freedom 🏆

Check out my regular articles on Motley Fool UK 📚

Follow me on social media, for daily financial education and market insights. 👏

Summary 📝

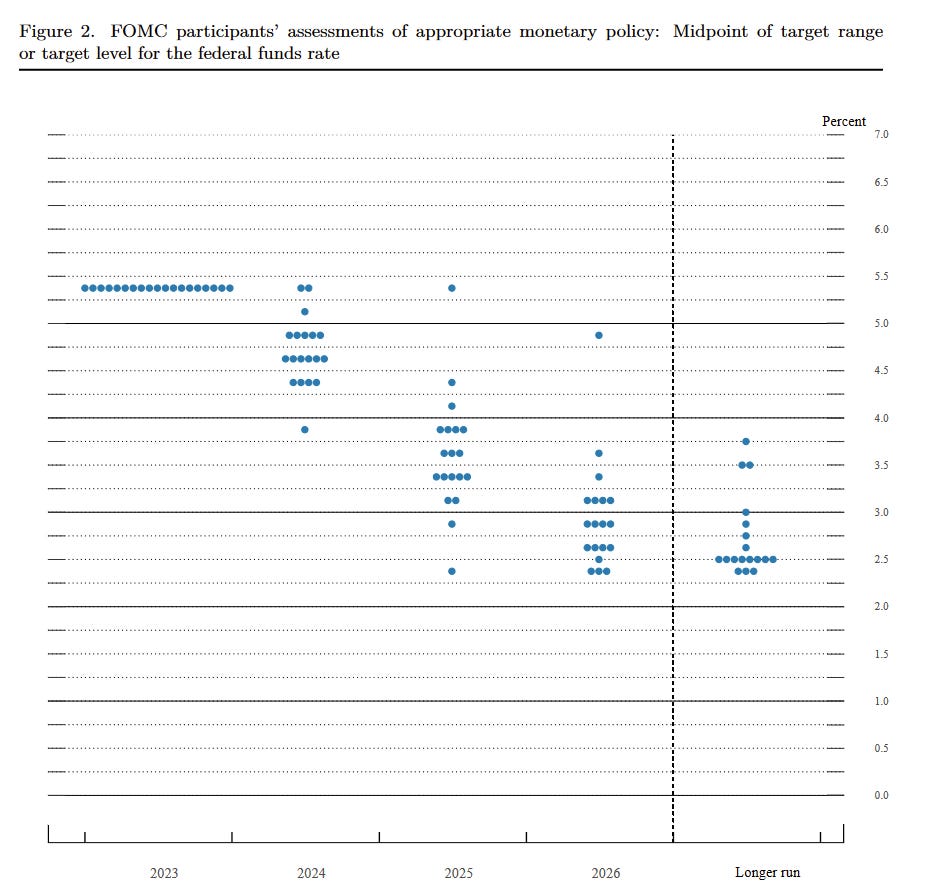

Yet ANOTHER green week as the Santa Rally continues into the end of the year. As expected, the US Federal Reserve paused it’s hiking regime of interest rates, with several cuts in rates projected for 2024.

So what were the main events from last week?

The Fed’s DotPlot shows us that estimates of rates over the next few years have clearly calmed down, with the majority of the heavy work now done.

Market Summary

S&P 500 SPY 0.00%↑- 2.74%

NASDAQ QQQ 0.00%↑- 3.30%

Dow Jones Industrial Average DJIA 0.00%↑- 2.90%

The Volatility Index fell throughout the week, ending substantially down as markets continued to move past interest rate fears and inflation concerns.

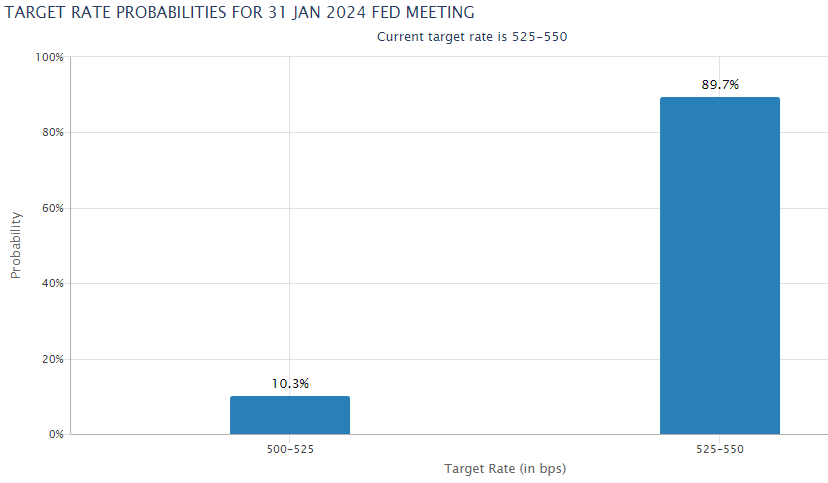

At present, markets are pricing in a 89.7% chance of no change in rates at the next Fed meeting in late January, with a 10.3% chance of 25BPS cut!

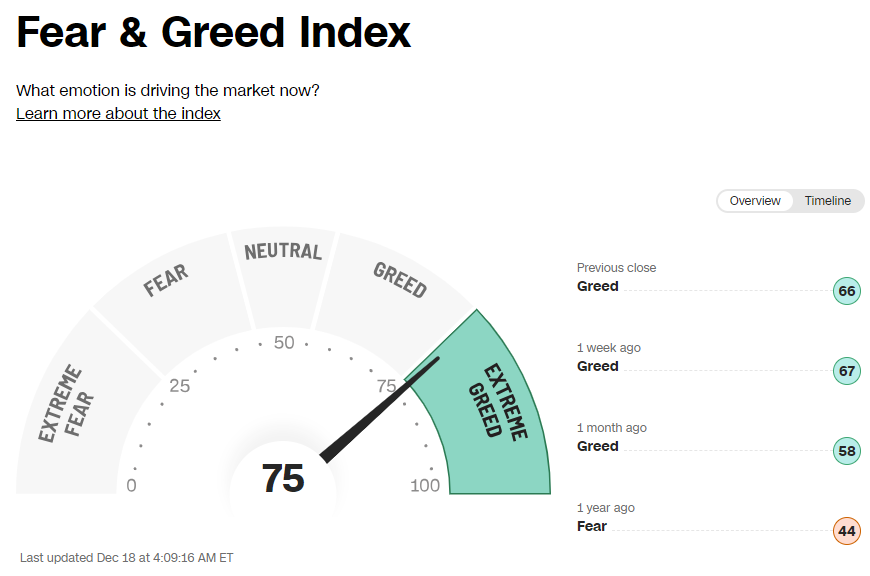

The Fear and Greed index climbed into Extreme Greed category at 75/100 for the first time since late August.

As I noted last time, seasonality is never far from my mind at this time of year, and it looks like the market is thinking the same thing despite some negative headlines. The average across the last 20 years has been great for the next few months, and many institutions seemingly don’t want to miss out!

Of course, nothing is a guarantee these days, but as always, if you keep to your strategy, don’t let the noise change your plan, and learn as much as you can, you can’t go too wrong over the long term!

In the meantime, have a fantastic Christmas for those celebrating, and have some well earned time off from the market, we’ve earned it!

This Week in History 📰

Source- The History Place

December 18, 1956 - Japan was admitted to the United Nations.

December 21st - Winter begins in the Northern Hemisphere. In the Southern Hemisphere today is the beginning of summer.

December 21, 1993 - The KGB (Soviet Secret Police) organization was abolished by Russian President Boris Yeltsin.

What’s on my Watchlist? 👀

Three stocks I think have an interesting week ahead.

Although not many companies are reporting, I suspect that FDX 0.00%↑ , NKE 0.00%↑ and CCL 0.00%↑ are all likely to be big movers this week.

What’s Moving Markets? 🏃♂️

Three stories I’ve got my eye on this week. Sourced from CNBC.

Russia-Ukraine live updates: Putin says Russia has no interest in fighting NATO; EU to pass 12th package of sanctions against Moscow

Landmark national security trial opens in Hong Kong for prominent activist publisher Jimmy Lai

Jimmy Lai, Apple Daily founder, arrives at the Court of Final Appeal ahead a bail hearing on February 9, 2021 in Hong Kong.

10-year Treasury yield slip further after Fed’s ‘big shift’

Major Events This Week 🔬

Economic Events

Source- Unusual Whales

Monday

10:00 am Home builder confidence index

Tuesday

8:30 am Housing starts

8:30 am Building permits

Wednesday

8:30 am U.S. current account

10:00 am Existing home sales

Thursday

8:30 am Initial jobless claims

8:30 am GDP (revision)

8:30 am Philadelphia Fed manufacturing survey

10:00 am U.S. leading economic indicators

Friday

8:30 am Durable-goods orders

8:30 am Durable-goods minus transportation

8:30 am Personal income

8:30 am Personal spending

8:30 am PCE index

8:30 am Core PCE index

8:30 am PCE (year-over-year)

8:30 am Core PCE (year-over-year)

10:00 am New home sales

10:00 am Consumer sentiment (final)

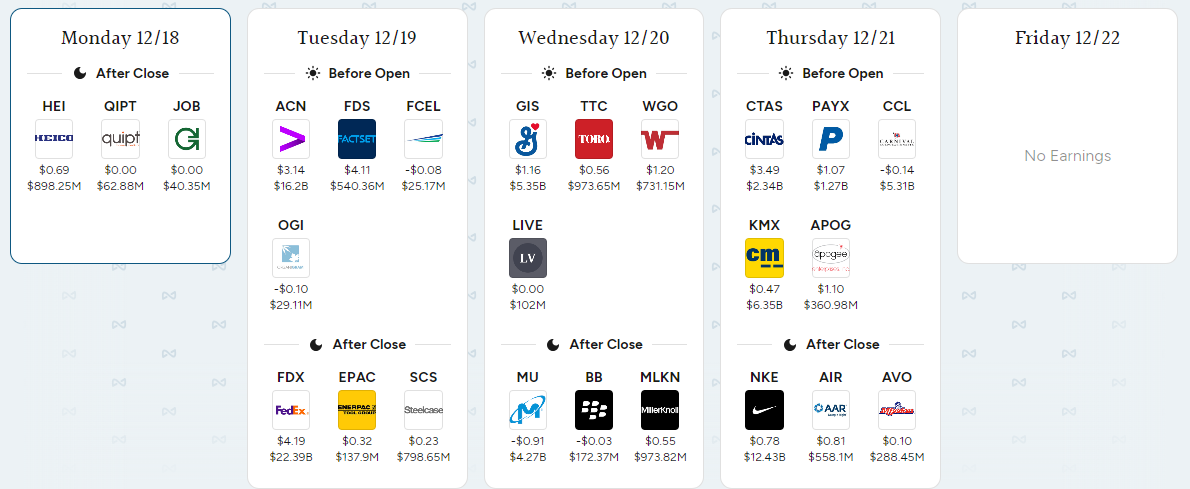

Incoming Earnings Reports

Source- Savvy Trader

Notable Upcoming Earnings

Monday

HEI (afterhours) Implied Move: +/- 5.28% Sector: Industrials

Tuesday

FDS (premarket) Implied Move: +/- 4.96% Sector: Financial Services

FDX (afterhours) Implied Move: +/- 4.42% Sector: Industrials

Wednesday

GIS (premarket) Implied Move: +/- 4.01% Sector: Consumer Defensive

MU (afterhours) Implied Move: +/- 4.73% Sector: Technology

Thursday

CCL (premarket) Implied Move: +/- 7.08% Sector: Consumer Cyclical

KMX (premarket) Implied Move: +/- 7.68% Sector: Consumer Cyclical

CTAS (premarket) Implied Move: +/- 4.57% Sector: Industrials

NKE (afterhours) Implied Move: +/- 5.18% Sector: Consumer Cyclical

Volatility Watch 🔥

Provided by Seeking Alpha.

Monday - December 18

Volatility watch - Options trading volume is high again on Spirit Airlines (SAVE) as traders wait on the result of the Department of Justice trial on blocking the merger with JetBlue Airways (JBLU). Sirius XM Holdings (SIRI) and Big Lots (BIG) both have an elevated level of short positions on them. The most overbought stocks per their 14-day Relative Strength Index are Snap (SNAP), Impact Fusion International (OTCPK:IFUS), and MBIA (MBI). The most oversold stocks per their 14-day Relative Strength Index are ReAlpha Tech (AIRE), Ventyx Bio (VTYX), and Talon Metals (OTCPK:TLOFF). Gold stocks Newmont (NEM), Barrick Gold (GOLD), Franco-Nevada (FNV), Coeur Mining (CDE), New Gold (NGD), Gold Fields Limited (GFI), Sibanye Stillwater Limited (SBSW), and i-80 Gold Corp. (IAUX) are some of the sector names on watch for more volatility.

Earnings watch - Notable companies due to report include HEICO (HEI).

All day - The Bank of America Hydrogen Conference will include presentations by Plug Power (PLUG) and CF Industries (CF).

Tuesday - December 19

Earnings watch - Notable companies due to report include FedEx (FDX), Accenture (ACN), FactSet (FDS), and FuelCell Energy (FCEL).

M&A votes - Livent (LTHM) shareholders will vote on the merger of equals with Allkem Limited (OTCPK:OROCF). Orchard Therapeutics (ORTX) shareholders will vote on the takeover offer from Kyowa Kirin (OTCPK:KNBWY) (OTCPK:KYKOY).

All day - The Bank of Japan meeting next week has the potential for some dramatic hints on the end of the negative interest rates era for the nation.

All day - WTI crude December futures will expire. Crude oil futures (CL1:COM) have seen extra volatility over the last year on contract expiration dates.

All day - AutoZone (AZO), United Natural Foods (UNFI), and Guidewire Software (GWRE) will hold their annual meetings.

8:30 a.m. The housing sector will get a double dose of data with the release of the building permits and housing starts reports.

12:30 p.m. Federal Reserve Bank of Atlanta President Raphael Bostic will speak on the U.S. economy and general business outlook.

5:30 p.m. FedEx (FDX) will hold its FQ4 earnings conference call. The stocks with the highest trading correlation with FedEx (FDX) on its earnings day are United Parcel Service (UPS), Expeditors International (EXPD), and Landstar System (LSTR).

Wednesday - December 20

Earnings watch - Notable companies due to report include General Mills (GIS), Micron Technology (MU), Toro (TTC), and Winnebago (WGO). Options trading on Blackberry (BB) implies a 9% swing in share price after the company reports.

10:00 a.m. The November existing home sales report will be released. Economists forecast 3.77M existing home sales in the month vs. 3.79M in October. Although mortgage rates are dropping, the 30-year fixed mortgage rate was still above 7% in November.

5:00 p.m. Micron Technology (MU) will hold its FQ1 earnings call. Options trading implies a 6% swing in share price after the semiconductor company reports. Qualcomm (QCOM) and FormFactor (FORM) are the two stocks with the tightest trading correlation to Micron on earnings days.

Thursday - December 21

Earnings watch - Notable companies due to report include CarMax (KMX), Paychex (PAYX), Carnival (CCL), and Nike (NKE). Options trading on Mission Produce (AVO) implies a 13% swing in share price after the company reports.

8:30 a.m. The Philadelphia Fed Index report will be released. Economists expect the index to stay in contractionary territory as business investment slows from the prior unsustainable level of growth.

4:30 p.m. ARK Invest will hold its December Fund mARKet Update webinar.

Friday - December 22

All day - The FDA action arrives for Ionis Pharmaceuticals' (IONS) Eplontersen for hereditary transthyretin-mediated amyloid polyneuropathy. The drug candidate met all primary and secondary endpoints in a phase 3 trial at 66 weeks. Ionis is teaming up with AstraZeneca (AZN) to develop and commercialize eplontersen

All day - It is the preliminary proxy deadline for the proposed merger between Alaska Airlines (ALK) and Hawaiian Holdings (HA).

8:30 a.m. The PCE core prices report will be released. The Federal Reserve's favored inflation gauge is forecast to show a soft 0.2% month-over-month and 3.4% year-over-year rise for November.

8:30 a.m. The November Durable Goods Orders report is forecast to show a small month-over-month increase, with Boeing (BA) expected to be less of a drag on the overall number than in October.

8:30 a.m. One of the final readings of the year on consumer sentiment will arrive just as the holiday shopping season wraps up. The University of Michigan Consumer Sentiment report is expected to be consistent with the preliminary reading, which showed a surge in sentiment to 69.4 from 61.3 previously amid confidence that interest rates will fall in 2024.

Seeking Alpha editor Josh Fineman contributed to this story

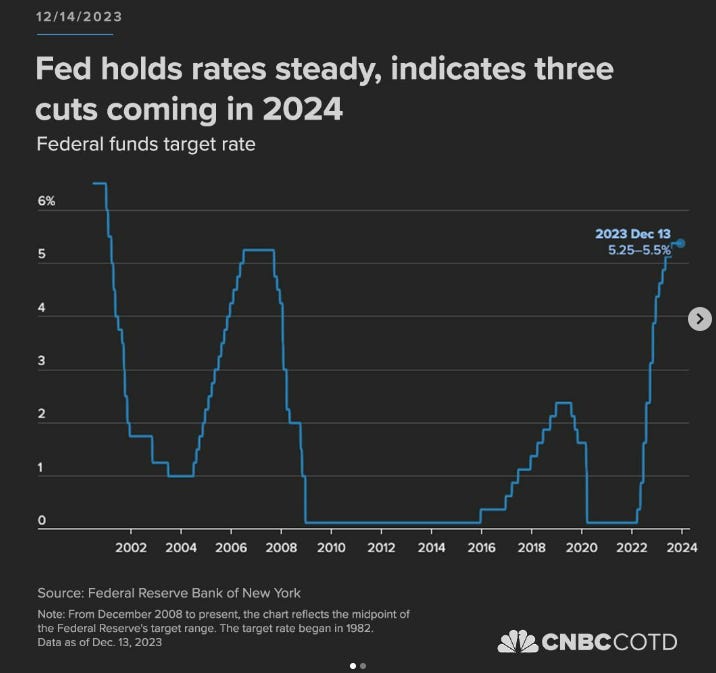

Chart of the Week 📈

Source- Chart of the Day

The Federal Reserve on Wednesday held its key interest rate steady for the third straight time and set the table for multiple cuts to come in 2024 and beyond.

With the inflation rate easing and the economy holding in, policymakers on the Federal Open Market Committee voted unanimously to keep the benchmark overnight borrowing rate in a targeted range between 5.25%-5.5%.

Along with the decision to stay on hold, committee members penciled in at least three rate cuts in 2024, assuming quarter percentage point increments.

Investor’s Toolkit ⚒️

Unusual Whales- Options Flow and Analysis 🛠

5% off with code OAK2022

SimplyWallSt- Stock Analysis 🛠

5% Discount with code OAK

Follow for More 🎉

Thanks for reading, have a great day!

Gordon

Disclosure ✅

This newsletter provides general information only. Before making any financial or investment decisions, please consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.