The Acorn 🌳#57

The Acorn 🌳#57

All you need to understand the market this week 📈💰

Monday, January 22nd 2024

Welcome to another recap on the week’s action and events!

I hope you enjoy this week’s recap, please get in touch if there’s anything more you’d like to see in The Acorn. If you like what you see, please like, subscribe and share to keep growing the Oak Investor community! 🌳

Thanks,

Gordon

Sponsor 🤝

This week’s newsletter is brought to you by Shares.io.

Become a smarter investor with Shares. Access more than 1,500 US stocks and connect with fellow investors.

This is a promotional content from which I may earn a commission. T&Cs and fees apply. Capital at risk.

Summary 📝

The S&P reached an all time high last week!

Despite continued uncertainty around interest rates, geopolitics, and inflation, the markets seem to be looking into the distance, and surging higher! This can be a dangerous combination, since the best case scenario is always a little ambitious, but if rates can cool down and companies can go back to thinking about their operations instead of the wider economy, the good times could well be back!

Market Summary

S&P 500 SPY 0.00%↑+ 1.2%

NASDAQ QQQ 0.00%↑+ 2.3%

Dow Jones Industrial Average DJIA 0.00%↑+ 0.7%

VIX Volatility Index +9.9%

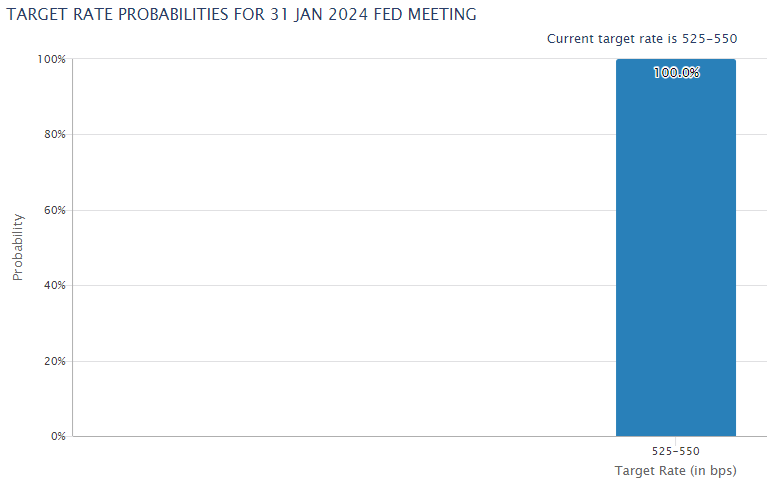

At present, markets are pricing in a 100% chance of no change in rates at the next Fed meeting in late January.

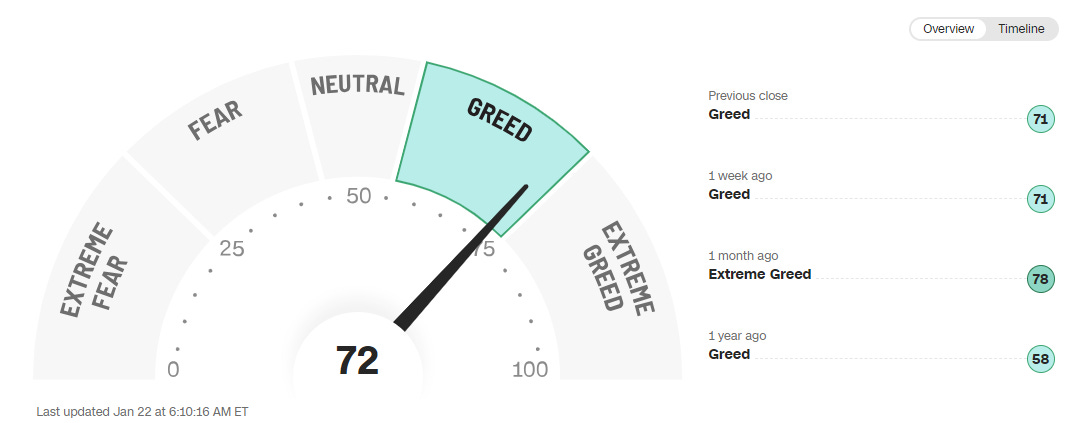

Despite the volatility, the Fear and Greed index remained in the Extreme Greed category at 72/100.

Investing at all time highs isn’t always easy, but if you’re willing to commit to a long-term strategy of regularly investing, history shows us that you’ll do just fine!

This Week in History 📰

Source- The History Place

January 22, 1901 - Queen Victoria of England died after reigning for 64 years, the longest reign in British history, during which England had become the most powerful empire in the world.

January 24, 1848 - The California gold rush began with the accidental discovery of the precious metal near Coloma during construction of a Sutter's sawmill.

January 26, 1788 - The British established a settlement at Sydney Harbor in Australia as 11 ships with 778 convicts arrived, setting up a penal colony to relieve overcrowded prisons in England.

What’s on my Watchlist? 👀

Three stocks I think have an interesting week ahead.

As earnings season gets into full swing, I expect the usual tech companies to provide a little excitement. I’ve got my eye on NFLX 0.00%↑, TSLA 0.00%↑, and IBM 0.00%↑.

What’s Moving Markets? 🏃♂️

Three stories I’ve got my eye on this week. Sourced from CNBC.

Two important events this week could determine the future of Fed rate policy

in New York City, U.S., January 19, 2024. REUTERS/Brendan McDermid")

Two big economic reports coming up this week could go a long way toward determining at least which way the central bank policymakers could lean on policy.

Gross domestic product will be released Thursday and the personal consumption expenditures prices reading on inflation is out Friday.

″ “It’s not about secret meetings or decisions. It’s fundamentally about the data” that will determine policy, Chicago Fed President Austan Goolsbee told CNBC.

India’s consumption growth is set to accelerate as Goldman predicts ‘affluent’ Indians to nearly double

India’s consumer sector is becoming key to the country’s economic growth, with consumption expected to accelerate amid rising disposable incomes.

Around 100 million people in India will earn more than $10,000 a year by 2027, according to Goldman Sachs.

There is a great desire to spend on travel, jewelry, eating out, among other things, with discretionary spending in the country on the rise, said McKinsey & Company’s Abhishek Malhotra.

Moody’s is negative on Asia’s sovereign creditworthiness in 2024 as China growth slows

adjusts the Philippines flag before the 51st Association of Southeast Asian Nations (ASEAN)- Republic of Korea Ministerial Meeting in Singapore on August 3, 2018. - Leaders, ministers and representatives are meeting in the city-state from August 1 to 4 for the ASEAN Ministerial Meeting (AMM). (Photo by Mohd RASFAN / AFP) (Photo credit should read MOHD RASFAN/AFP via Getty Images)")

Moody’s Investors Service has a negative outlook for sovereign creditworthiness in Asia-Pacific this year, due to China’s slower economic growth as well as tight funding and geopolitical risks.

The credit rating agency said the slowdown in China’s growth “significantly influences” APAC economies because of China’s strong integration to global supply chains.

“This is also predicated on global liquidity conditions where we really don’t see the Fed easing until the middle of the year,” said Christian De Guzman, senior vice president at Moody’s Investors Service.

Major Events This Week 🔬

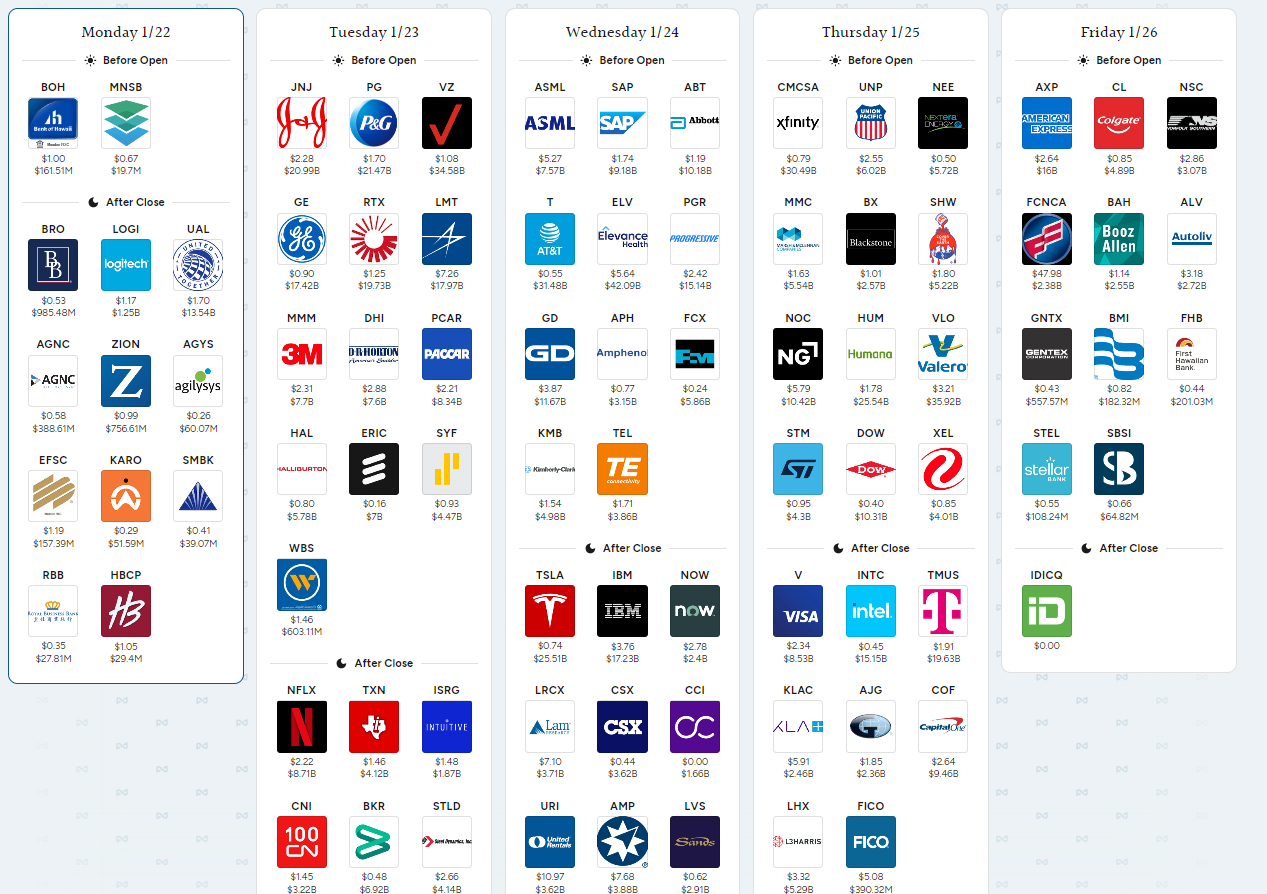

Incoming Earnings Reports

Source- Savvy Trader

Catalyst Watch 🔥

Source- Seeking Alpha.

Monday - January 22

Volatility watch - Options trading volume is still high on Spirit Airlines (SAVE) following the news that the DOJ blocked its merger with JetBlue Airways (JBLU). The regulatory shadow in the airline sector is also impacting trading on merger partners Hawaiian Holdings (HA) and Alaska Airlines (ALK). Annovis Bio (ANVS) has also seen more options bets placed on it recently than normal activity. Virgin Galactic (SPCE) and EVgo (EVGO) both have an elevated level of short interest outstanding on them ahead of the earnings season. The most overbought stocks per their 14-day Relative Strength Index include Phunware (PHUN), Juniper (JNPR), and Drone Delivery Canada (OTCQX:TAKOF). The most oversold stocks per their 14-day Relative Strength Index include Spirit Airlines (SAVE), PNM Resources (PNM), and Alternus Clean Energy (ALCE).

Central bank watch - Interest rate decisions are due in this week from the Bank of Japan, European Central Bank, and the Bank of Canada. In the U.S., Federal Reserve members will be in a blackout period of no public talks ahead of the next FOMC meeting on January 30-31.

Earnings watch - Notable companies due to report include Brown & Brown (BRO), United Airlines Holdings (UAL), and Zions Bancorporation (ZION).

All week - In the crypto world, the Roundhill Bitcoin Covered Call Strategy ETF (YBTC) will begin its second week of trading as the only actively managed bitcoin covered call strategy ETF in the U.S. The fund aims to capture bitcoin price action and provide income from a covered call strategy.

All day - The blackout period begins for Federal Reserve members in advance of the January 30-31 meeting.

All day - BJ’s Restaurants (BJRI), Xponential Fitness (XPOF), and First Watch Restaurant Group (FWRG) will be participating in the Jefferies Consumer Summit.

All day - WTI crude February futures will expire. Crude oil futures (CL1:COM) have seen extra volatility over the last year on contract expiration dates.

10:00 a.m. Darling Ingredients (DAR) will hold a Webinar titled "A Closer Look at RFS RIN Market and the Outlook for RD-SAF Projects."

Tuesday - January 23

Earnings watch - Notable companies due to report include Johnson & Johnson (JNJ), Procter & Gamble (PG), Netflix (NFLX), Verizon Communications (VZ), Texas Instruments (TXN), General Electric (GE), and Lockheed Martin (LMT). Options trading implies large share price moves for Stride (LRN) and MakeMyTrip Limited (MMYT) after their reports.

All day - The three-day TD Securities Global Mining Conference will include participation from Arizona Sonoran Copper Company (OTCQX:ASCUF), Endeavor Group Holdings (EDR), E3 Lithium Limited (ETL:CA), Lithium Royalty Corp. (LIRC:CA), Pan American Silver Corp. (PAAS), Piedmont Lithium (PLL), 10x Genomics (TXG), and Wheaton Precious Metals (WPM).

All day - Shareholders with EngageSmart (ESMT) will vote on the buyout offer from Vista Equity.

8:30 a.m. Procter & Gamble (PG) will hold its earnings call. The update from the consumer staples giant could have widespread sector implications. Analysts have warned that the household products landscape has evolved since P&G raised their organic revenue growth and EPS targets to the high end of the initial range in October. Kimberly-Clark (KMB) is the stock that has correlated the tightest to P&G's stock on earnings day over the last two years.

Wednesday - January 24

Earnings watch - Notable companies due to report include Tesla (TSLA), Abbott Laboratories (ABT), IBM (IBM), AT&T (T), General Dynamics (GD), Las Vegas Sands (LVS), and CSX (CSX). Options trading implies large share price moves for SL Green Realty (SLG) and Monro (MNRO) after their reports.

All day - The FDA action date arrives for Liquidia Corporation's (LQDA) for its Yutrepia inhalation powder. The FDA has previously confirmed that Liquidia may add the treatment of PH-ILD to the label for YUTREPIA without additional clinical studies.

All day - The Nasdaq will release its latest update on short interest positions.

12:00 p.m. Jack in the Box (JACK) will hold its 2024 Investor Day event with presentations scheduled from top management.

5:30 p.m. Tesla (TSLA) will hold its earnings conference call. The electric vehicle sector will be on watch to see what Elon Musk and gang say about 2024 production expectations and the margin outlook, with average selling prices falling. Options trading implies a swing in share price of 7% after the Tesla earnings report is released. Notably, Tesla fell 9% after its last earnings report. The stocks that have correlated the closest to Tesla on earnings day over the two years are Rivian Automotive (RIVN) and Polestar Automotive (PSNY).

Thursday - January 25

Earnings watch - Notable companies due to report include Visa (V), Intel (INTC), Comcast (CMCSA), Union Pacific (UNP), American Airlines Group (AAL), and Southwest Airlines (LUV). Options trading implies large share price moves for Levi Strauss (LEVI) and Alaska Air Group (ALK) after they report.

All day - Investor events include annual meetings for Walgreens Boots Alliance (WBA), Spire (SR), Jabil (JBL) and Post Holdings (POST).

All day - Porsche (OTCPK:POAHY) (OTCPK:VLKAF) will unveil the all-Electric Macan SUV after a series of delays. The 2024 Macan EV will feature a new electric platform that will also underpin the upcoming Audi A6 e-tron. A dual-motor powertrain is expected to produce up to 603 horsepower.

8:15 a.m. The European Central Bank will issue a monetary policy statement.

8:30 a.m. The Durable Goods Orders report for December will be released. Economists expect a 0.5% increase.

Friday - January 26

Earnings watch - Notable companies due to report include American Express (AXP), Colgate-Palmolive (CL), Norfolk Southern (NSC), and Autoliv (ALV).

All day - The termination date will arrive for the Spirit Airlines (SAVE)-JetBlue Airways (JBLU) merger, although the agreement is expected to be extended.

8:30 a.m. The core PCE price index will be released. Economists forecast the inflation gauge will show a 0.2% month-over-month and 2.9% year-over-year increase. The forecast implies the first sub-3.0% year-over-year reading for core PCE since March of 2021.

Seeking Alpha editor Josh Fineman contributed to this story

Chart of the Week 📈

Source- Chart of the Day

The stock market has its dips, but it has always bounced back. And generally speaking, someone with money invested in the stock market will be better off in the long run than someone who just held onto their cash.

One reason is because cash loses purchasing power over time due to inflation. Anyone who pays attention to prices can tell you the same $20 does not go as far at the grocery store today as it did in 2019.

Stashing money in a savings account that earns a little interest is a step up. But with a national average interest rate of less than 1% on regular savings accounts, according to Bankrate, it’s still not enough to beat inflation.

The S&P 500, on the other hand, has seen average annual returns of 10% over the last 50 years. So even in a “bad” year, you’re probably better off having some of your money invested rather than all in savings.

Want to Work with Me? 📈

If you’d like to take your investing to the next level, there are 4 ways I can help:

Pick up a free 40 page copy of It’s Only Investing, and get started with investing! 📚

Pick up the comprehensive, 150 page The Investor’s Blueprint, and learn at your own pace 📚

Book a free discovery call with me, and discuss how you can take a step closer to financial freedom 🏆

Check out my regular articles on Motley Fool UK 📚

Follow me on social media, for daily financial education and market insights. 👏

X/Twitter 🐣

YouTube 🎥

LinkedIn 💻

Thanks for reading, have a great day!

Gordon

Disclosure ✅

This newsletter provides general information only. Before making any financial or investment decisions, please consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.