The Acorn 🌳#58

The Acorn 🌳#58

All you need to understand the market this week 📈💰

Monday, January 29th 2024

Welcome to another recap on the week’s action and events!

I hope you enjoy this week’s recap, please get in touch if there’s anything more you’d like to see in The Acorn. If you like what you see, please like, subscribe and share to keep growing the Oak Investor community! 🌳

Thanks,

Gordon

Summary 📝

A mixed week for stocks last week, but overall the market continued to move higher as earnings season saw TSLA 0.00%↑ disappoint, NFLX 0.00%↑ soar, and plenty more movement!

Market Summary

S&P 500 SPY 0.00%↑+ 0.8%

NASDAQ QQQ 0.00%↑+ 0.4%

Dow Jones Industrial Average DJIA 0.00%↑+ 0.5%

VIX Volatility Index +3.1%

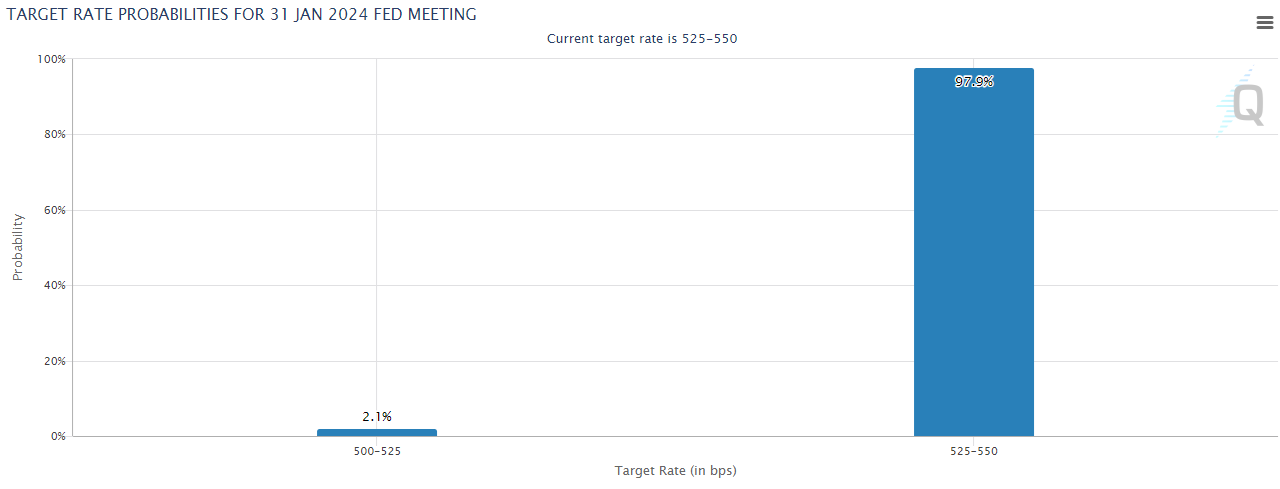

At present, markets are pricing in a 97.9% chance of no change in rates at the next Fed meeting in late January, with a tiny chance of a cut by 25BPS.

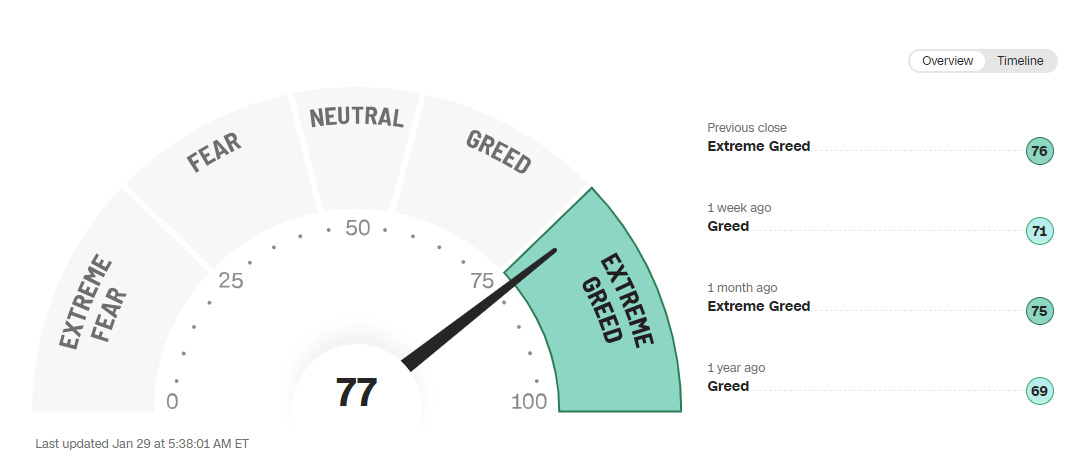

Despite the volatility, the Fear and Greed index remained in the Extreme Greed category at 76/100.

This week promises to be another busy one, with an interest rate decision from the US Fed, more earnings from MSFT 0.00%↑ AAPL 0.00%↑ GOOGL 0.00%↑ and AMZN 0.00%↑.

As I said last week, investing at all time highs isn’t always easy, but if you’re willing to commit to a long-term strategy of regularly investing, history shows us that you’ll do just fine!

This Week in History 📰

Source- The History Place

February 1, 2003 - Sixteen minutes before it was scheduled to land, the Space Shuttle Columbia broke apart in flight over west Texas, killing all seven crew members.

February 2, 1990 - In South Africa, the 30-year-old ban on the African National Congress was lifted by President F.W. de Klerk, who also promised to free Nelson Mandela and remove restrictions on political opposition groups.

February 3, 1870 - The 15th Amendment to the U.S. Constitution was ratified, guaranteeing the right of citizens to vote, regardless of race, color, or previous condition of servitude.

What’s on my Watchlist? 👀

Three stocks I think have an interesting week ahead.

As earnings season gets into full swing, I expect the usual tech companies to provide a little excitement. I’ve got my eye on AMZN 0.00%↑ AAPL 0.00%↑ and following last week’s slump, movement from TSLA 0.00%↑.

What’s Moving Markets? 🏃♂️

Three stories I’ve got my eye on this week. Sourced from CNBC.

A handful of space companies are running out of cash and time. Here are three at risk

While many space companies battened the hatches to survive, a few publicly-traded names are running on fumes.

A trio of names appear likely going the way of Virgin Orbit, which flamed out last year: Momentus, Astra and Sidus Space.

Despite some likely turbulence ahead, the space sector as a whole isn’t necessarily struggling.

China’s luxury market is bouncing back. Analysts say these are new areas of opportunity

LVMH results showed that despite some resumption of overseas travel, more of China’s consumers are buying luxury products at home.

The mainland China personal luxury market grew by about 12% last year to more than 400 billion yuan ($56.43 billion), according to consulting firm Bain & Company.

In all, about half the leading brands and several niche brands, have rebounded to 2021 sales levels, the Bain report said, without sharing specific names.

")

Evergrande shares halted after Hong Kong court orders liquidation

Shares of China Evergrande were briefly halted after plunging over 20% in early trading.

Hong Kong court decision comes after it was reported that Evergrande’s overseas creditors failed to reach an 11th-hour deal this weekend to restructure.

Major Events This Week 🔬

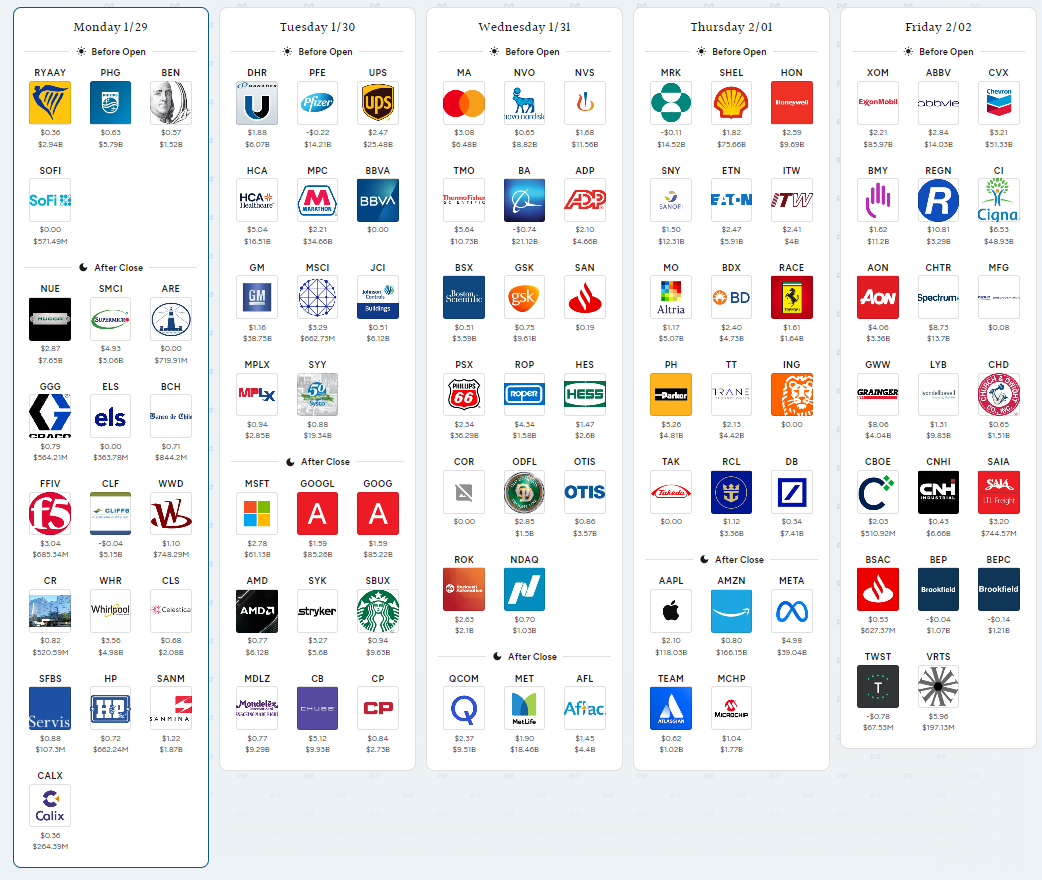

Incoming Earnings Reports

Source- Savvy Trader

Notable Upcoming Earnings

Monday

SOFI (premarket) Implied Move: +/- 15.21% Sector: Financial Services

CLF (afterhours) Implied Move: +/- 5.54% Sector: Basic Materials

SMCI (afterhours) Implied Move: +/- 10.37% Sector: Technology

Tuesday

PFE (premarket) Implied Move: +/- 3.85% Sector: Healthcare

GM (premarket) Implied Move: +/- 4.39% Sector: Consumer Cyclical

JBLU (premarket) Implied Move: +/- 11.22% Sector: Industrials

AMD (afterhours) Implied Move: +/- 8.10% Sector: Technology

GOOGL (afterhours) Implied Move: +/- 4.65% Sector: Communication Services

MSFT (afterhours) Implied Move: +/- 3.98% Sector: Technology

SBUX (afterhours) Implied Move: +/- 4.98% Sector: Consumer Cyclical

Wednesday

BA (premarket) Implied Move: +/- 4.12% Sector: Industrials

MA (premarket) Implied Move: +/- 2.82% Sector: Financial Services

QCOM (afterhours) Implied Move: +/- 5.13% Sector: Technology

Thursday

PTON (premarket) Implied Move: +/- 14.44% Sector: Consumer Cyclical

MRK (premarket) Implied Move: +/- 2.33% Sector: Healthcare

SHEL (premarket) Implied Move: +/- 2.36% Sector: Energy

AAPL (afterhours) Implied Move: +/- 3.11% Sector: Technology

AMZN (afterhours) Implied Move: +/- 5.68% Sector: Consumer Cyclical

META (afterhours) Implied Move: +/- 6.03% Sector: Communication Services

X (afterhours) Implied Move: +/- 0.87% Sector: Basic Materials

Friday

XOM (premarket) Implied Move: +/- 2.57% Sector: Energy

CVX (premarket) Implied Move: +/- 2.61% Sector: Energy

ABBV (premarket) Implied Move: +/- 3.00% Sector: Healthcare

Catalyst Watch 🔥

Source- Seeking Alpha.

Monday - January 29

Volatility watch - Options trading volume is elevated on Spirit Airlines (SAVE) as traders gauge the impact of the DOJ blocking the merger with JetBlue Airways (JBLU). ProKidney Corp. (PROK) and Fisker (FSR) both have an elevated level of short interest outstanding on them ahead of the earnings season. The most overbought stocks per their 14-day Relative Strength Index include Dave (DAVE), Kaman (KAMN), and RayzeBio (RYZB). The most oversold stocks per their 14-day Relative Strength Index include reAlpha Tech (AIRE), Archer-Daniels-Midland (ADM), and Alternus Clean Energy (ALCE).

Earnings watch - Notable companies due to report include Whirlpool (WHR) and Nucor (NUE).

All day - Baker Hughes (BKR) will hold its annual meeting in Florence, Italy. The list of speakers includes top Baker Hughes executives, representatives from Saudi Aramco (ARMCO), and the Saudi energy minister.

All day - Rocket Lab USA (RKLB) could see some action following the weekend launch of its Electron rocket on behalf of Spire Global and NorthStar Earth & Space. The space launch stock is down almost 9% for the early part of 2024.

All day - The listing for Flutter Entertainment (OTCPK:PDYPY) on the New York Stock Exchange is expected to become effective. The trading symbol for Flutter in the U.S. will be FLUT.

All day - Hub Group (HUBG) will begin trading on a split-adjusted basis following the company's 2-for-1 stock split.

Tuesday - January 30

Earnings watch - Notable companies due to report include General Motors (GM), UPS (UPS), Sysco (SYY), Pfizer (PFE), Alphabet (GOOG), Microsoft (MSFT), Starbucks (SBUX), Mondelez International (MDLZ), and AMD (AMD). Options trading implies large share price moves for Teradyne (TER) after it reports.

All day - Arcos Dorados (ARCO) will be on watch as the company participates in the Bradesco BBI Retail Days event in São Paulo. Shares of ARCO have rallied in the past after the McDonald's (MCD) franchisee operator updated on strategy at the event.

10:00 a.m. JetBlue Airways (JBLU) will hold its earnings conference call amid high drama over the attempt to buy out Spirit Airlines (SAVE).

Wednesday - January 31

Earnings watch - Notable companies due to report include Phillips 66 (PSX), Boeing (BA), Mastercard (MA), MetLife (MET), and Qualcomm (QCOM). Options trading implies large share price moves for Regis (RGS) and Wolfspeed (WOLF) after their reports.

All day - Sports equipment company Amer Sports is expected to start trading after pricing its IPO. The Finland-based company owns iconic sports and outdoor brands that include Arc’teryx, Salomon, Wilson, Atomic, Louisville Slugger, and Peak Performance.

All day - The FDA action date will arrive on priority review of Sanofi (SNY) and Regeneron Pharmaceuticals' (REGN) label expansion for their blockbuster drug Dupixent (dupilumab) to treat children aged 1 to 11 years with eosinophilic esophagitis. Dupixent will be the first and only FDA-approved treatment for EoE in children of this age group if approved.

All day - The ImmunoGen (IMGN)-AbbVie (ABBV) merger goes to a shareholder vote. The buyout of Consolidated Communications (CNSL) by Searchlight Capital Partners and British Columbia Investment Management will also be voted on. CNSL traded about 6% below the deal price at publication time.

10:30 a.m. Boeing (BA) will hold its earnings conference call. Executives will be on the hot seat amid the Boeing Max 9 grounding and investors are likely to get new guidance to factor in.

2:00 p.m. The Federal Reserve will make its policy statement issued at the conclusion of the meeting of the Federal Open Market Committee. The consensus expectation is that interest rates will be held steady and that only very subtle changes will be made to the policy statement.

2:30 p.m. Federal Reserve Chairman Jerome Powell will hold a press conference.

Thursday - February 1

Earnings watch - Notable companies due to report include Merck (MRK), Honeywell (HON), Altria (MO), Amazon (AMZN), Apple (AAPL), Meta Platforms (META), Royal Caribbean (RCL), and Post Holdings (POST). Options trading implies large share price moves for Peloton Interactive (PTON) and Canada Goose (GOOS) after they report.

All day - Investor events include a Texas Instruments (TXN) business update call, Oculis (OCS) presenting at the Next Generation Ophthalmic Drug Delivery Summit, and annual meetings for PriceSmart (PSMT) and Amdocs (DOCS).

All day - Sodexo S.A. (OTCPK:SDXAY) plans to spin off its benefits and rewards business into a new company. Pluxee is described as a global player in the employee benefits and engagement market, with an established presence in 31 countries. Shares will trade on the Euronext Paris exchange.

10:00 a.m. Texas Instruments (TXN) will host a capital management review event. Shares of TXN have been volatile in the past when the event was held.

Friday - February 2

Earnings watch - Notable companies due to report include Exxon Mobil (XOM), Chevron (CVX), AbbVie (ABBV), and Charter Communications (CHTR).

8:30 a.m. The jobs report for January will be released. Economists anticipate a strong level of 180K job additions for the month, down from the 210K job adds in December. The unemployment rate is expected to tick up to 3.8%. Average hourly earnings are forecast to be up 4.1% year-over-year.

Seeking Alpha editor Josh Fineman contributed to this story

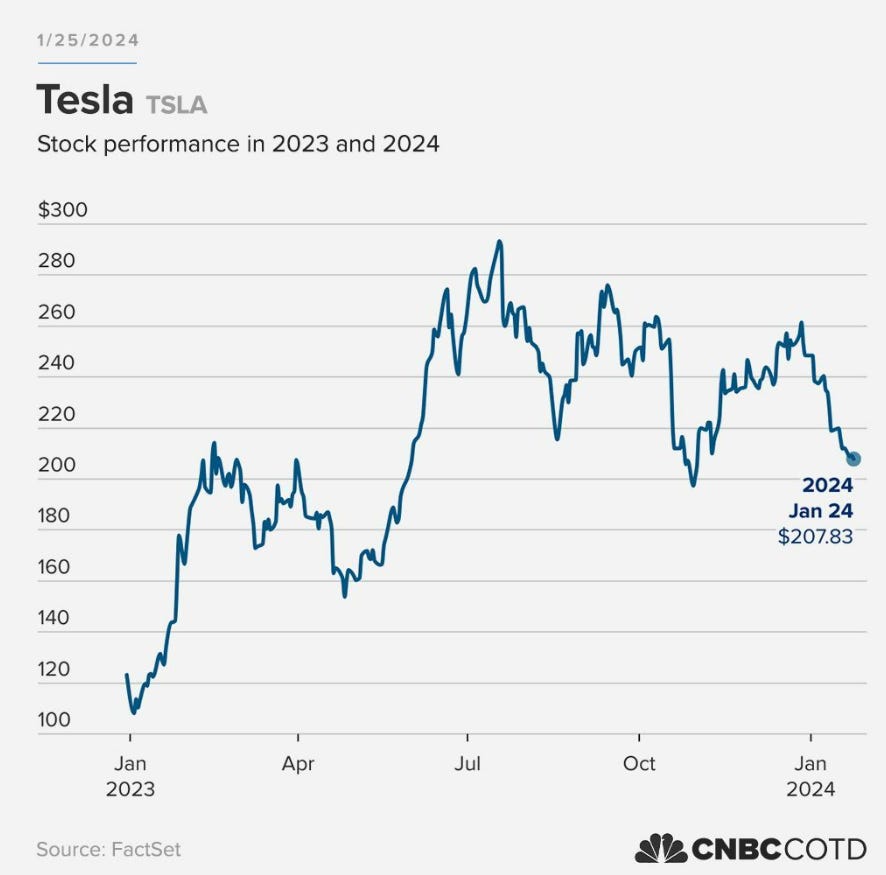

Chart of the Week 📈

Source- Chart of the Day

Tesla reported revenue and profit for the fourth quarter that missed analysts’ estimates as automotive revenue increased just 1% from a year earlier.

Total revenue increased 3% from $24.3 billion a year earlier. Operating margin for the quarter came in at 8.2%, down from the year-ago quarter’s figure of 16% and slightly higher than 7.6% in the prior quarter.

Meager growth in auto revenue was partly due to a reduced average selling price following steep price cuts around the world in the second half of the year. Net income for the quarter more than doubled to $7.9 billion, or $2.27 per share, from $3.7 billion, or $1.07 per share, a year earlier. The increase was mostly due to a $5.9 billion one-time noncash tax benefit.

Want to Work with Me? 📈

If you’d like to take your investing to the next level, there are 4 ways I can help:

Pick up a free 40 page copy of It’s Only Investing, and get started with investing! 📚

Pick up the comprehensive, 150 page The Investor’s Blueprint, and learn at your own pace 📚

Book a free discovery call with me, and discuss how you can take a step closer to financial freedom 🏆

Check out my regular articles on Motley Fool UK 📚

Follow me on social media, for daily financial education and market insights. 👏

X/Twitter 🐣

YouTube 🎥

LinkedIn 💻

Thanks for reading, have a great day!

Gordon

Disclosure ✅

This newsletter provides general information only. Before making any financial or investment decisions, please consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.

Keeps getting better and better 👍