The Acorn 🌳#59

The Acorn 🌳#59

All you need to understand the market this week 📈💰

Monday, February 5th 2024

Welcome to another recap on the week’s action and events!

I hope you enjoy this week’s recap, please get in touch if there’s anything more you’d like to see in The Acorn. If you like what you see, please like, subscribe and share to keep growing the Oak Investor community! 🌳

Thanks,

Gordon

Sponsor

This week’s newsletter is brought to you by SavingsRates.org

At Oak Investing, we firmly believe that knowledge is power when it comes to your money. Let’s check out some key stats:

The average savings account gets 0.46% interest, while rates are available over 5%.

Over 10 years, the average savings account will lose $2,500 per year in interest.

Investing is a great way to build wealth. The market grew over 20% in 2023, and has averaged 12% growth every year for the last 10 years.

By using SavingsRates to check what’s out there for your savings account and investment portfolio, your money can be working SO much harder, taking you closer to financial freedom!

Summary 📝

Another week of all time highs for the S&P 500, as tech earnings saw META 0.00%↑ soar over 20%, and many other large cap companies roaring higher. Solid jobs numbers indicated the US economy is in a good place, and many central banks around the world indicated another pause in interest rates.

All of the above leads to a moment of optimism in the market, where both economy and market appear to be in a good place, with hope that 2024 can be another year where the recession many predicted is avoided.

Market Summary

S&P 500 SPY 0.00%↑+ 1.3%

NASDAQ QQQ 0.00%↑+ 1.1%

Dow Jones Industrial Average DJIA 0.00%↑+ 1.4%

VIX Volatility Index +3.5%

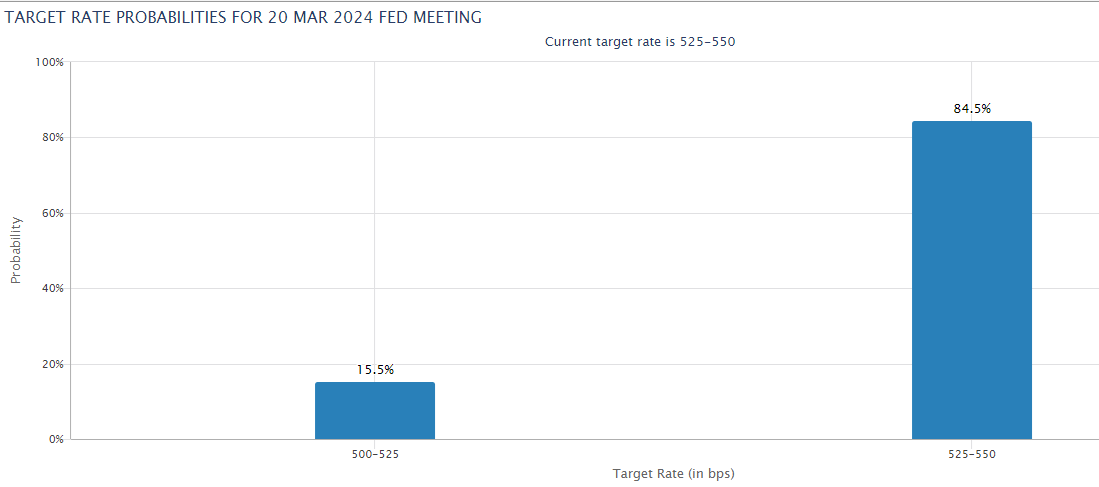

At present, markets are pricing in a 85% chance of no change in rates at the next Fed meeting in late March, with a small chance of a cut by 25BPS.

The Fear and Greed index dropped back down into the Greed category at 70/100.

Earnings season continues this week, with reports from more of the world’s biggest companies. Technology earnings showed us that investment is continuing, and confidence is generally high, but as we move into retail and the more consumer focussed sectors, all eyes will be on whether this confidence can be maintained!

This Week in History 📰

Source- The History Place

February 5, 1917 - The new constitution of Mexico, allowing for sweeping social changes, was adopted.

February 6, 1952 - King George VI of England died. Upon his death, his daughter Princess Elizabeth became Queen Elizabeth II, Queen of the United Kingdom of Great Britain and Northern Ireland.

February 11, 1929 - Italian dictator Benito Mussolini granted political independence to Vatican City and recognized the sovereignty of the Pope (Holy See) over the area, measuring about 110 acres.

What’s on my Watchlist? 👀

Three stocks I think have an interesting week ahead.

More focus on earnings reports, with BABA 0.00%↑ and PLTR 0.00%↑ likely to be big movers. I also have my eye on DKNG 0.00%↑ as Superbowl fever takes over for the weekend.

What’s Moving Markets? 🏃♂️

Three stories I’ve got my eye on this week. Sourced from CNBC.

Turkey’s inflation sees biggest monthly jump since August, nears 65% year-on-year

In January, Turkish inflation logged its biggest monthly jump since August with a 6.7% rise from December, while year-on-year inflation hit nearly 65%.

Food, beverages and tobacco, as well as transportation, all increased between roughly 5% and 7% month-on-month, while housing was up 7.4% since December.

The figures come two days after Turkey’s appointment of a new central bank governor, Fatih Karahan.

Gold prices to hit $2,200 and a ‘dramatic’ outperformance awaits silver in 2024, says UBS

Gold and silver are expected to climb further in 2024 on expectations that the U.S. Federal Reserve will start cutting interest rates, UBS forecasts.

As interest rates dip, gold becomes more appealing compared to alternative investments like bonds.

Powell insists the Fed will move carefully on rate cuts, with probably fewer than the market expects

Federal Reserve Chair Jerome Powell vowed in a “60 Minutes” interview aired Sunday that the central bank will proceed carefully with interest rate cuts this year.

“We just want some more confidence before we take that very important step of beginning to cut interest rates,” he said.

Powell warned that the monetary policy tightening would cause “some pain.” However, “it really hasn’t happened,” he added.

Major Events This Week 🔬

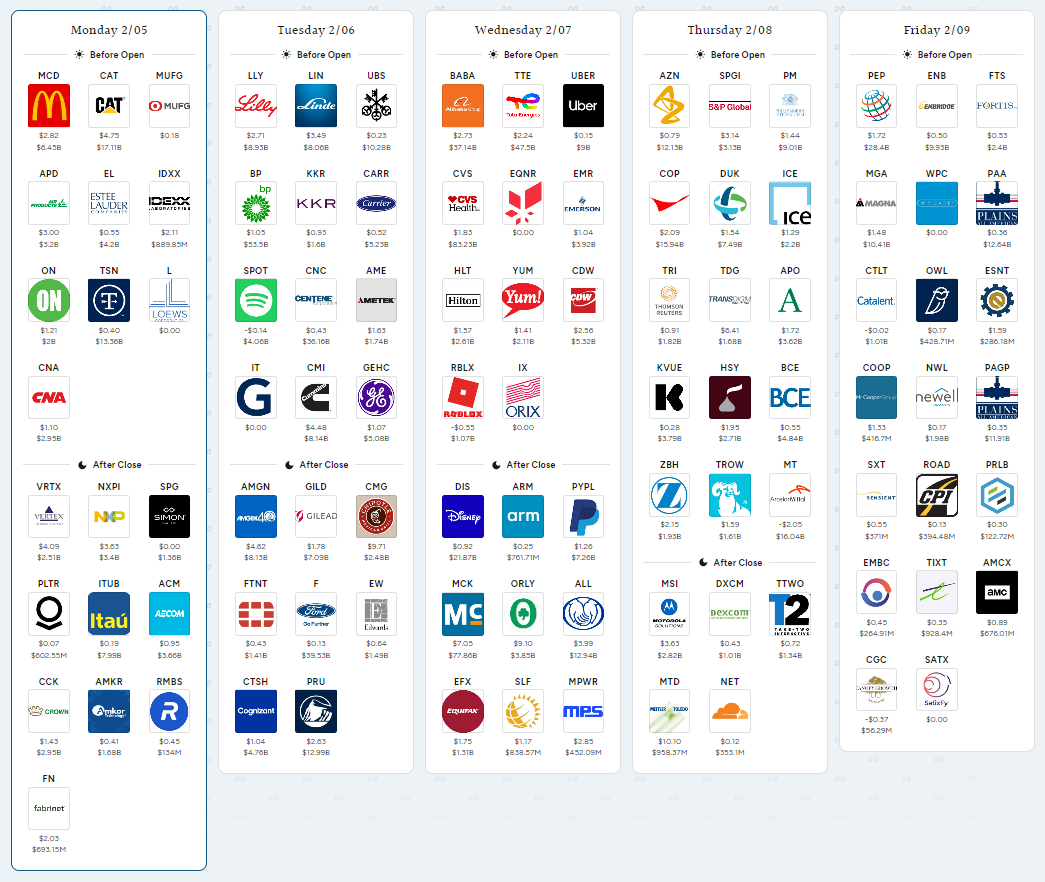

Incoming Earnings Reports

Source- Savvy Trader

Catalyst Watch 🔥

Source- Seeking Alpha.

Monday - February 5

Volatility watch - Options trading volume and short interest are still high on B. Riley Financial (RILY). The most overbought stocks per their 14-day relative strength index include Selina Hospitality (SLNA), RayzeBio (RYZB), and Vera Therapeutics (VERA). The most oversold stocks per their 14-day Relative Strength Index include L. Catterton Asia Acquisition (LCAA), Chenghe Acquisition (CHEA), and iRobot (IRBT).

Earnings watch - Notable companies due to report include McDonald's (MCD), Caterpillar (CAT), Vertex Pharmaceuticals (VRTX), Tyson Foods (TSN), NXP Semiconductors (NXPI), and Estee Lauder (EL).

All day - The World Defense Show will continue in Saudi Arabia. Companies scheduled to participate include General Dynamics (GD), BAE Systems (OTCPK:BAESF), Lockheed Martin (LMT), Airbus (OTCPK:EADSF), Boeing (BA), Northrop Grumman (NOC), and L3Harris (LHX). As part of its presence, Boeing (BA) will present a virtual-reality display of the F-15EX cockpit, demonstrating the advanced multi-role fighter aircraft’s state-of-the-art design and technologies; and the T-7A Red Hawk Advanced Pilot Training System simulator, highlighting the ground-based training system of Boeing’s next-generation training jet.

All day - The Federal Reserve will release its Senior Loan Officer Opinion Survey on bank lending practices.

All day - Deadline for Fury to find escrow for Battalion Oil (BATL) deal.

2:00 p.m. Atlanta Federal Reserve Bank President Raphael Bostic will give welcome remarks before the virtual "Uneven Outcomes in the Labor Market" conference hosted by the Federal Reserve Board of Governors.

Tuesday - February 6

Earnings watch - Notable companies due to report include Eli Lilly (LLY), Toyota Motor (TM), Centene (CNC), Amgen (AMGN), Ford Motor (F), and BP (BP). Options trading implies large share price moves for Snap (SNAP), e.l.f. Beauty (ELF), and Spotify Technologies (SPOT) after their reports.

12:00 p.m. Cleveland Federal Reserve Bank President Loretta Mester will give a keynote before the Ohio Bankers League Economic Summit.

12:00 p.m. BigBear.ai (BBAI) will host an investor presentation that will include updates on the company’s planned acquisition of Pangiam.

Wednesday - February 7

Earnings watch - Notable companies due to report include Alibaba (BABA), CVS Health (CVS), Fox Corporation (FOXA), McKesson (MCK), Disney (DIS), Uber Technologies (UBER), PayPal (PYPL) and Spirit Airlines (SAVE). Options trading implies double-digit share price moves for Arm Holdings (ARM) and Roblox (RBLX) after their reports.

All day - Shareholders with Pioneer Natural Resources (PXD) will vote on the proposed merger with Exxon Mobil (XOM).

All day - The Manheim Used Car Price Index report will be released. The update on the used car market is relevant for Carvana (CVNA), CarMax (KMX), Lithia Motors (LAD), AutoNation (AN), Asbury Automotive Group (ABG), CarGurus (CARG), Group 1 Automotive (GPI), Sonic Automotive (SAH), Penske Automotive Group (PAG), Vroom (VRM), Shift Technologies (OTC:SFTGQ), and Cars.com (CARS).

11:30 a.m. Allogene Therapeutics (ALLO) will participate in the Guggenheim Healthcare Talks Biotechnology Conference.

12:00 p.m. Richmond Federal Reserve Bank President Thomas Barkin to participate in conversation before the Economic Club of Washington D.C.

9:00 p.m. - Hollysys Automation (HOLI) shareholders will vote on sale to Ascendent.

Thursday - February 8

Earnings watch - Notable companies due to report include Capri Holdings (CPRI), ConocoPhillips (COP), Philip Morris (PM), Duke Energy (DUK), Expedia (EXPE), Take-Two Interactive (TTWO), Tapestry (TPR), Pinterest (PINS), and Kenvue (KVUE). Options trading implies large share price moves after they report.

9:00 a.m. Mineralys Therapeutics (MLYS) Chief Executive Officer Jon Congleton will be participating in a fireside chat at the Guggenheim Securities Biotechnology Conference.

10:00 am. Spirit Airlines (SAVE) will hold a conference call on Q4 results.

6:15 p.m. F5 (FFIV) will host a strategy and product session for investors and financial analysts in connection with F5’s premier application security and delivery conference, AppWorld 2024.

Friday - February 9

Earnings watch - Notable companies due to report include PepsiCo (PEP), Newell Brands (NWL), and AMC Networks (AMCX).

All day - CPI seasonal factors will be revised, which could result in revisions to seasonally adjusted inflation data.

All day - The Chicago Auto Show will begin. The long list of vehicles on display includes the Acura ADX, BMW i4, BMW i7, BMW ix, BMW x5, Cadillac Escalade IQ, Cadillac Lyriq, Chevrolet Blazer EV, Chevrolet Equinox EV, Chevrolet Silverado EV, Ford e-Transit, Ford F-150 Lightning, Ford Mustang Mach-E, GMC Hummer EV, GMC Sierra EV, Honda Prologue, Hyundai Ioniq 5, Hyundai Ioniq 6, Hyundai Kona, Kia EV6, Kia Niro, Lexus RZ, Lucid (LCID) Air, Nissan Ariya, Volkswagen ID.4, Volkswagen ID.7, and Volkswagen ID.Buzz.

All day -It is the last trading before the Chinese New Year begins. The extended holiday could be a boost for Macau-related stocks such as Melco Resorts & Entertainment (MLCO), MGM Resorts (MGM), Las Vegas Sands (LVS), and Wynn Resorts (WYNN).

All day - Super Bowl buzz will be hitting a peak, which could mean some extra attention for sports betting stocks such as DraftKings (DKNG), MGM Resorts (MGM), Flutter Entertainment (FLUT) in front of the high-profile game that is anticipated to smash betting records.

Seeking Alpha editor Josh Fineman contributed to this story

Chart of the Week 📈

Source- Chart of the Day

Job growth posted a surprisingly strong increase in January, demonstrating again that the U.S. labor market is solid and poised to support broader economic growth.

Nonfarm payrolls expanded by 353,000 for the month, much better than the Dow Jones estimate for 185,000, the Labor Department’s Bureau of Labor Statistics reported Friday. The unemployment rate held at 3.7%, against the estimate for 3.8%.

Want to Work with Me? 📈

If you’d like to take your investing to the next level, there are 4 ways I can help:

Pick up a free 40 page copy of It’s Only Investing, and get started with investing! 📚

Pick up the comprehensive, 150 page The Investor’s Blueprint, and learn at your own pace 📚

Book a free discovery call with me, and discuss how you can take a step closer to financial freedom 🏆

Check out my regular articles on Motley Fool UK 📚

Follow me on social media, for daily financial education and market insights. 👏

X/Twitter 🐣

YouTube 🎥

LinkedIn 💻

Thanks for reading, have a great day!

Gordon

Disclosure ✅

This newsletter provides general information only. Before making any financial or investment decisions, please consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.