The Acorn 🌳#60

The Acorn 🌳#60

All you need to understand the market this week 📈💰

Monday, March 4th 2024

Welcome to another recap on the week’s action and events!

I hope you enjoy this week’s recap, please get in touch if there’s anything more you’d like to see in The Acorn. If you like what you see, please like, subscribe and share to keep growing the Oak Investor community! 🌳

Thanks,

Gordon

Sponsor

This week’s newsletter is brought to you by SavingsRates.org

At Oak Investing, we firmly believe that knowledge is power when it comes to your money. Let’s check out some key stats:

The average savings account gets 0.46% interest, while rates are available over 5%.

Over 10 years, the average savings account will lose $2,500 per year in interest.

Investing is a great way to build wealth. The market grew over 20% in 2023, and has averaged 12% growth every year for the last 10 years.

By using SavingsRates to check what’s out there for your savings account and investment portfolio, your money can be working SO much harder, taking you closer to financial freedom!

Summary 📝

Markets continued to move upwards following more bullish news in the semiconductor sector, and as crypto continued to rally!

Market Summary

S&P 500 SPY 0.00%↑+ 0.9%

NASDAQ QQQ 0.00%↑+ 1.65%

Dow Jones Industrial Average DJIA 0.00%↑-0.15%

VIX Volatility Index -2.9%

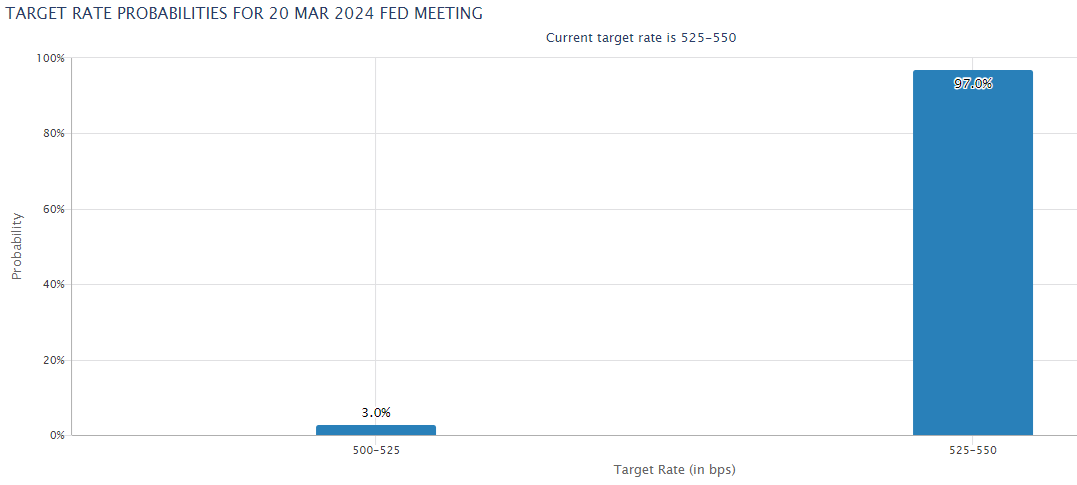

At present, markets are pricing in a 97% chance of no change in rates at the next Fed meeting in late March, with a small 3% chance of a cut by 25BPS.

The Fear and Greed index stayed in the Extreme Greed category at 79/100.

Seasonality continues to be a hot topic as markets continue to roar. I never want to be stuck with volatile assets as the music stops, especially when all the metrics are suggesting that investors might be getting ahead of themselves.

The great data from Unusual Whales shows this well:

We see that March can be hit or miss with the market, but generally positive as optimism grows, winter ends, and people begin to make plans for the year ahead. Now can be a great time to put your money to work, but knowing that we’ve seen a VERY bullish run in the last few months, so a slowdown wouldn’t be a huge surprise!

As always, stick to your strategy, and make sure your money is working as hard as you are!

This Week in History 📰

Source- The History Place

March 4, 1681 - King Charles II of England granted a huge tract of land in the New World to William Penn to settle an outstanding debt. The area later became Pennsylvania.

March 5, 1933 - Amid a steadily worsening economic situation, newly elected President Franklin D. Roosevelt proclaimed a four-day "Bank Holiday" to stop panic withdrawals by the public and the possible collapse of the American banking system.

March 10, 1862 - The first issue of U.S. government paper money occurred as $5, $10 and $20 bills began circulation.

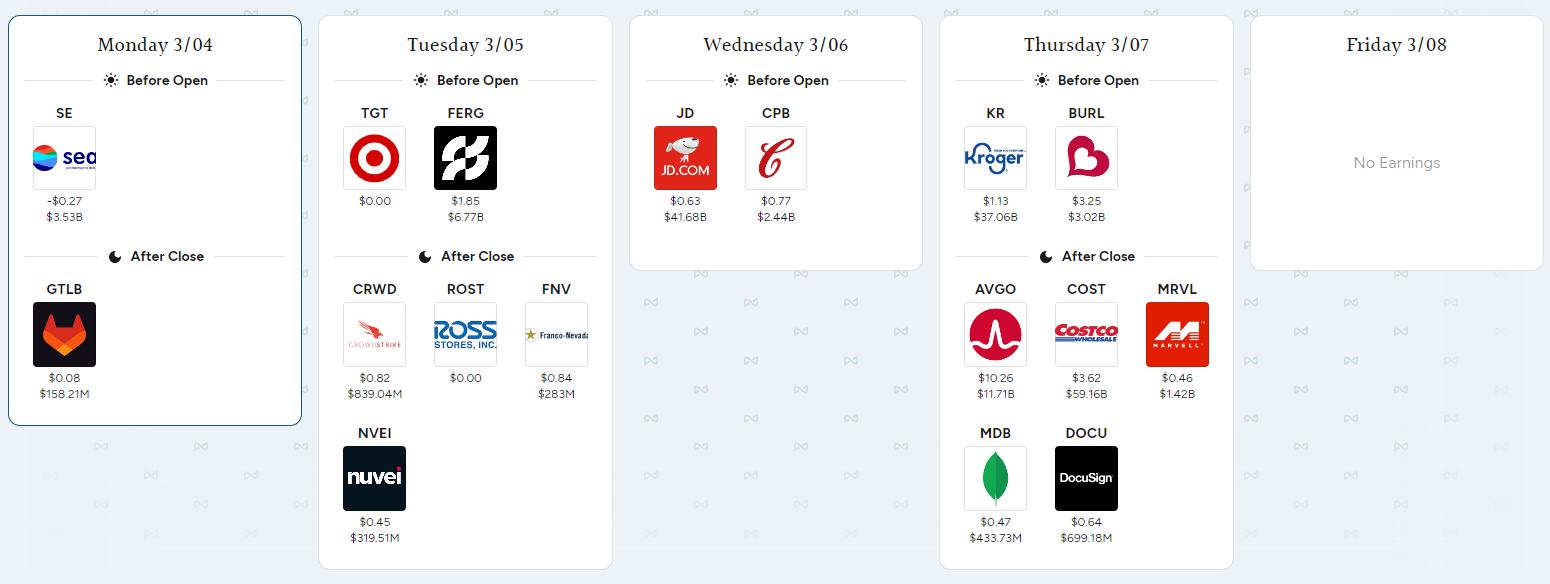

What’s on my Watchlist? 👀

Three stocks I think have an interesting week ahead.

More volatile reports expected from several companies this week. I’ve got my eye on NIO 0.00%↑ CRWD 0.00%↑ and SEA 0.00%↑ for big moves.

What’s Moving Markets? 🏃♂️

Three stories I’ve got my eye on this week. Sourced from CNBC.

‘Last chance saloon’: UK finance minister expected to pledge pre-election tax cuts

Heading into what will likely be the Conservative government’s last fiscal event before the country’s upcoming general election, Hunt is under pressure to offer a sweetener to voters.

His party trails the main opposition Labour Party by more than 20 points across all national polls.

Deutsche Bank estimates that the government’s fiscal headroom will have grown from around £13 billion ($16.46 billion) to around £18.5 billion, and sees tax cuts as “very likely” the first port of call.

Japan’s Nikkei closes above 40,000 after Wall Street benchmarks hit record highs; China ‘Two Sessions’ meeting in focus

The index ended 0.5% higher at 40,109.23, while the broader Topix fell 0.12%, retreating from its all-time high hit on Friday.

China breaks with tradition at annual ‘Two Sessions’ meeting by scrapping premier’s press conference

, to mark 10th anniversary of the Belt and Road Initiative, in Beijing, China October 18, 2023. REUTERS/Edgar Su/File Photo")

China is set this week to kick off its annual parliamentary meetings, which investors are watching closely for signals on economic stimulus.

China’s economic policy is typically set at an annual meeting in December by leaders within the ruling Communist Party of China.

The meetings this month, known as the “Two Sessions,” are at the government, instead of party, level and typically release more details on policy plans, such as the GDP target for the year.

Major Events This Week 🔬

Incoming Earnings Reports

Source- Savvy Trade

Catalyst Watch 🔥

Source- Seeking Alpha.

Monday - March 4

Volatility watch - Options trading volume is still elevated on SoundHound AI (SOUN) and Barclays (BCS). The list of highly-shorted stocks heading into the new week includes Beyond Meat (BYND) and Cinemark Holdings (CNK). The most overbought stocks per their 14-day relative strength index include Viking Therapeutics (VKTX), Vivani Medical Inc (VANI), and Caret Holdings Inc (ROOT). The most oversold stocks per their 14-day Relative Strength Index include AN2 Therapeutics (ANTX), Semilux International (SELX), and SSR Mining (SSRM).

Earnings watch - Notable companies due to report include Sea Limited (SE), GitLab (GTLB) and Stitch Fix (SFIX).

9:10 a.m. Walgreens Boots Alliance (WBA) CEO Tim Wentworth and Global CFO Manmohan Mahajan will be presenting at the TD Cowen Health Care Conference.

9:15 a.m. Oshkosh Corporation (OSK) will participate in a fireside chat at Raymond James’ 45th Annual Institutional Investors Conference.

1:00 p.m. American Airlines Group (AAL) Chief Executive Officer Robert Isom and senior leadership will present at the company's Investor Day.

1:15 p.m. Nvidia (NVDA) will present at the Morgan Stanley Technology, Media and Telecom Conference.

4:25 p.m. Netflix (NFLX) will present at the Morgan Stanley Technology, Media and Telecom Conference.

Tuesday - March 5

Earnings watch - Notable companies due to report include Target (TGT), NIO (NIO), Ross Stores (ROST), Nordstrom (JWN), CrowdStrike (CRWD), and Box (BOX). Options trading implies double-digit share price moves for Hashicorp (HCP) and Vivid Seats (SEAT) after their reports.

Healthcare watch - AC Immune (ACIU) will have multiple presentations at the International Conference on Alzheimer’s and Parkinson’s Diseases. Vaxxinity (VAXX) will also present clinical data from its UB-312 program in Parkinson’s disease and preclinical data from its anti-tau program in Alzheimer’s disease at the International Conference on Alzheimer’s and Parkinson’s Diseases and related neurological disorders.

All day - Companies scheduled to participate in the Morgan Stanley Technology, Media and Telecom Conference include Palo Alto Networks (PANW), AMD (AMD), Disney (DIS), IMAX (IMAX), and Iron Mountain (IRM).

All day - Fisker (FSR) has an extraordinary shareholder meeting scheduled. Shareholders will vote on a stock issuance proposal and authorized shares proposal.

8:00 a.m. Nasdaq (NDAQ) will host its 2024 Investor Day. The event will feature presentations on the company’s operations and strategy, as well as question and answer sessions, with members of Nasdaq’s senior leadership team.

8:40 a.m. Target (TGT) will hold a financial community meeting following the release of its earnings report covering the holiday quarter. Some of the key topics of interest will be the initial FY24 guidance, the latest on cost savings efforts, indications of a subscription offering, and capital allocation priorities. Options trading implies a 7% swing in share price after the earnings report drops. The three stocks that correlate the closest to Target are Nordstrom (JWN), Abercrombie & Fitch (ANF), and Dollar Tree (DLTR).

12:30 p.m. NerdWallet (NRDS) Co-Founder & CEO Tim Chen will participate in a fireside chat at KeyBanc Capital Markets Emerging Technology Summit in San Francisco.

1:00 p.m. Super Micro (SMCI) will present at the KeyBanc Emerging Technology Summit.

Wednesday - March 6

Earnings watch - Notable companies due to report include JD.com (JD), Brown-Forman (BF.A), Campbell Soup (CPB), Foot Locker (FL), Abercrombie & Fitch (ANF), and Victoria's Secret (VSCO). Options trading implies double-digit share price moves for EVgo (EVGO) and Rush Street Interactive (RSI) after their reports.

All day - The Leap Conference in Riyadh, Saudi Arabia will include talks by ServiceNow (NOW) CEO Bill McDermott, Plug Power (PLUG) CEO Saeed Amidi, Aramco (ARMCO) CEO Amin Nasser, Zoom Video (ZM) CEO Eric Yuan, and TikTok CEO Shou Chew.

All day - Federal Reserve Chairman Jerome Powell will testify before the House Financial Services Committee.

All day - BetMGM (OTCPK:GMVHF) (MGM) CEO Adam Greenblatt will be one of the notable speakers at the NEXT Summit New York, which is described as North America’s premier iGaming and sports betting conference.

All day - GoDaddy (GDDY) will host an Investor Day at its Tempe, Arizona, headquarters. Key members of GoDaddy's management team will host a series of presentations and product demonstrations.

8:40 a.m. First Watch Restaurant (FWRG) will host a fireside chat at the Raymond James 2024 Institutional Investors Conference and meet with institutional investors.

9:10 a.m. Thermo Fisher Scientific (TMO) will present at the TD Cowen Health Care Conference. The company is going through the regulatory review process with its planned acquisition of Olink Holdings (OLK). Shares of Olink traded about 12.9% below the deal price at the time of publication.

All day - Companies scheduled to participate in the Morgan Stanley Technology, Media and Telecom Conference include Cerence (CRNC), Alphabet (GOOG), Intel (INTC), Shopify (SHOP), and Uber Technologies (UBER).

2:00 p.m. The Federal Reserve will release its Beige Book report.

Thursday - March 7

Earnings watch - Notable companies due to report include Kroger (KR), Bilibili (BILI), Costco (COST), Broadcom (AVGO), Gap (GPS), Marvell Technology (MRVL), and DocuSign (DOCU). Options trading implies large share price moves for Big Lots (BIG) and Bitfarms (BITF) after they report.

All day - Rivian Automotive (RIVN) will reveal its next-generation vehicle called the R2 at an event in Laguna Beach, California. The electric SUV model is expected to be smaller and cheaper than the R1S and R1T. The company has hinted that the model could be listed in the $40,000 to $60,000 range. Mass production of the R2 is not expected until 2026.

All day - General Electric Company (GE) will hold its GE Aerospace Investor Day event with the aerospace leadership team scheduled to present.

All day - Cigna Group (CI) will host its Investor Day in New York City.

All day - Federal Reserve Chairman Jerome Powell will deliver semiannual monetary policy testimony before the Senate Banking Committee.

7:45 a.m. The European Central Bank will hold a press conference following its rate announcement.

1:30 p.m. Cleveland Federal Reserve Bank President Loretta Mester will speak virtually on the economic outlook as part of the European Economics and Financial Centre's Distinguished Speaker Series.

2:00 p.m. Mattel (MAT) will host a Virtual Investor Presentation to provide a strategic business update and its plans for 2024.

5:00 p.m. VYNE Therapeutics (VYNE) Chief Scientific Officer Dr. Iain Stuart will deliver an oral presentation featuring positive data from the Phase 1b trial of VYN201 in vitiligo at the 2024 Global Vitiligo Foundation Annual Scientific Symposium taking place in San Diego.

Friday - March 8

Earnings watch - Notable companies due to report include Genesco (GCO) and America's Car-Mart (CRMT).

All day - The SXSW festival begins in Austin, Texas. For investors, the most interesting part of the festival could be the startup pitches from upstarts looking for funding. Participants in the past have been funded by large companies such as Google (GOOG), British Telecom, Apple (AAPL), Live Nation (LYV), OpenTable (BKNG), Meta Platforms (META), and Harmonic (HLIT).

8:30 p.m. The U.S. jobs report for February will be released. Economists expect 215K job additions for the month and for the unemployment rate to hold steady at 3.7%.

Seeking Alpha Editor Josh Fineman contributed to this story.

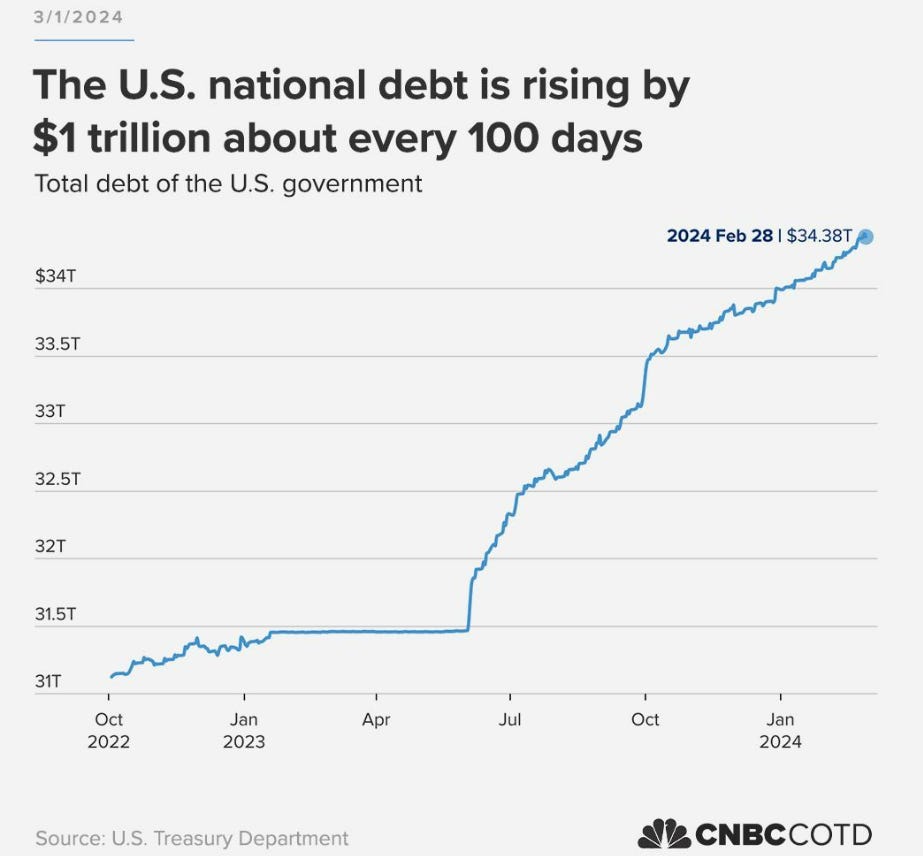

Chart of the Week 📈

Source- Chart of the Day

The debt load of the U.S. is growing at a quicker clip in recent months, increasing about $1 trillion nearly every 100 days.

The nation’s debt permanently crossed over to $34 trillion on Jan. 4, after briefly crossing the mark on Dec. 29, according to data from the U.S. Department of the Treasury. It reached $33 trillion on Sept. 15, 2023, and $32 trillion on June 15, 2023, hitting this accelerated pace. Before that, the $1 trillion move higher from $31 trillion took about eight months.

U.S. debt, which is the amount of money the federal government borrows to cover operating expenses, now stands at nearly $34.4 billion, as of Wednesday. Bank of America investment strategist Michael Hartnett believes the 100-day pattern will remain intact with the move from $34 trillion to $35 trillion.

Want to Work with Me? 📈

If you’d like to take your investing to the next level, there are 4 ways I can help:

Pick up a free 40 page copy of It’s Only Investing, and get started with investing! 📚

Pick up the comprehensive, 150 page The Investor’s Blueprint, and learn at your own pace 📚

Book a free discovery call with me, and discuss how you can take a step closer to financial freedom 🏆

Check out my regular articles on Motley Fool UK 📚

Follow me on social media, for daily financial education and market insights. 👏

X/Twitter 🐣

YouTube 🎥

LinkedIn 💻

Thanks for reading, have a great day!

Gordon

Disclosure ✅

This newsletter provides general information only. Before making any financial or investment decisions, please consult a financial planner to take into account your personal investment objectives, financial situation and individual needs.